{kind=link}

Why Investors Are Betting Big on Stablecoins and CBDCs

In recent years, the rise of stablecoins has strongly transformed the landscape of digital finance, with over $170 billion of these digital assets now held globally, according to CoinGecko.

Unlike traditional cryptocurrencies such as and , which are often criticised for their price volatility, stablecoins are designed to keep a steadier value by being pegged to reserve assets such as the US dollar or gold. This stability makes stablecoins increasingly appealing to both everyday investors and large institutions, creating a bridge between traditional finance and the fast-evolving world of digital assets.

The idea of a stable digital currency echoes the vision expressed by economist Friedrich Hayek in his 1976 work, The Denationalization of Money. Hayek proposed that a competitive market of private currencies, each backed by various assets, could promote a more stable and efficient monetary system than one controlled by governments. While Bitcoin represents a significant move towards Hayek’s ideal of a decentralized currency free from central authority, its volatility undermines its utility as a stable medium of exchange.

In contrast, stablecoins aim to realize Hayek’s vision by merging the stability of traditional currencies with the cutting-edge capabilities of blockchain technology. By offering a reliable store of value and a practical medium of exchange for everyday transactions, stablecoins address the volatility issues that have been one of the main criticisms of other cryptocurrencies.

This intersection of traditional finance and digital technology has not only attracted interest from governments, businesses, and individual users but also set the stage for a new era of financial interaction. As stablecoins continue to evolve and gain traction, they are set to play a pivotal role in reshaping how we think about and engage with money in the digital age.

The Evolution of Stablecoins

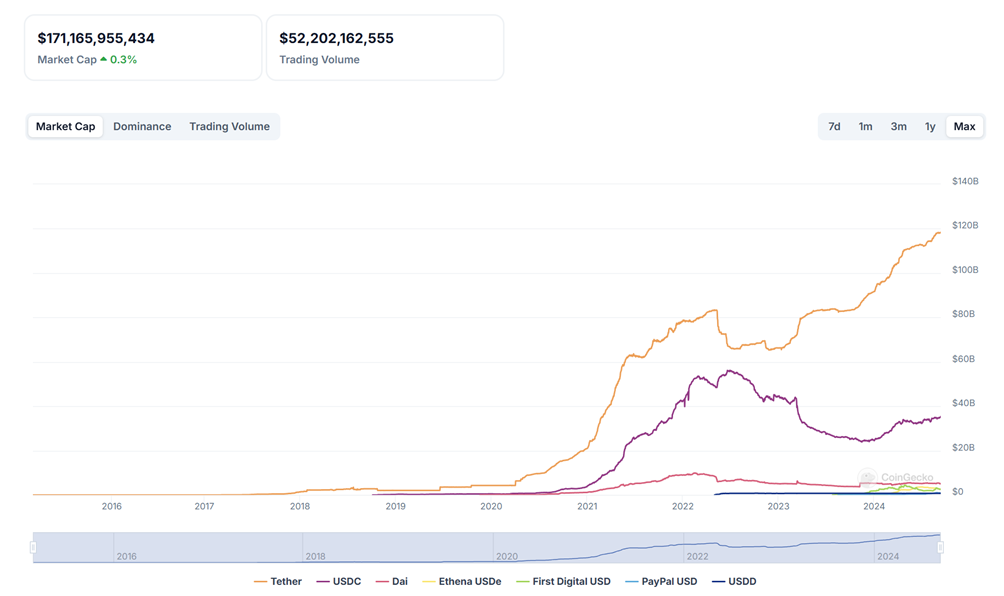

The mechanics behind stablecoins are diverse, reflecting the different approaches to achieving price stability. The most common type is fiat-collateralised stablecoins, which are backed by reserves of fiat currency held in a bank. For example, (USDT), the most widely used stablecoin, is pegged to the and claims to be backed by a reserve of assets equal in value to the amount of USDT in circulation. Tether’s market dominance, with a market share of 69% of the total market capitalization of all stablecoins according to Forbes, underscores the demand for a stable, dollar-pegged cryptocurrency.

Main stablecoins – Market cap over time

Source: CoinGecko

Another significant player in the stablecoin market is (USDC). Issued by the Centre Consortium, which includes companies like Circle and Coinbase (NASDAQ:), USDC is also pegged to the US dollar and is fully backed by dollar reserves.

Unlike Tether, USDC undergoes regular audits by independent accounting firms, providing an additional layer of trust for users. This transparency has made USDC a preferred choice for institutional investors and businesses looking to leverage stablecoins for everyday transactions, cross-border payments and DeFi applications, (as underlined by the increase of USDC market capitalisation growth of around 32% since September of 2023.

The algorithmic stablecoin is another innovative approach within this space. Unlike fiat-collateralised stablecoins, algorithmic stablecoins maintain their peg through algorithms that automatically adjust the supply of the token in response to market demand. TerraUSD (UST), which was one of the most prominent algorithmic stablecoins, maintained its peg by incentivising users to either mint or burn tokens based on the market price.

Although TerraUSD ultimately failed in maintaining its peg, leading to its collapse in 2022, the concept of algorithmic stablecoins remains a key area of interest and experimentation within the blockchain community. The failure of TerraUSD also highlighted the risks associated with algorithmic models, particularly in how they respond under stress conditions, prompting more rigorous debate and innovation in the sector.

Beyond these examples, the stablecoin landscape continues to evolve, with a range of new models and innovations being introduced. Hybrid stablecoins, which mix elements from both fiat-collateralised and algorithmic approaches, are gaining attention for their potential to balance decentralisation with stability.

This exploration of hybrid models is part of a broader trend where multi-collateralised stablecoins, backed by a diverse range of assets instead of just one, are being developed to spread risk and enhance resilience against market fluctuations. By using a variety of assets such as different fiat currencies, commodities, and cryptocurrencies, these stablecoins aim to minimise the impact of volatility in any single asset, providing greater stability and reducing the likelihood of significant value swings. Such innovations address the limitations of previous models by offering improved protection against economic shocks and contributing to overall stability.

These ongoing developments highlight that the stablecoin market is far from static. Developers and financial engineers are continually refining these digital assets to improve their resilience, efficiency, and broader adoption. As stablecoins gain in popularity, their integration into the mainstream financial system is becoming more pronounced, marking their increasing importance in both everyday transactions and complex financial applications. This dynamic evolution underscores the growing sophistication and centrality of stablecoins within the cryptocurrency ecosystem.

Financial Inclusion and Emerging Markets

Financial inclusion, the effort to make financial services affordable and accessible to all, remains a pressing challenge in many emerging economies. According to the World Bank, one of the main obstacles is the high cost of banking services, driven by limited competition and the dominance of a few large institutions.

Moreover, changing regulations around cross-border transactions have made it harder for banks to maintain remittance service partnerships. As the Bank for International Settlements (BIS) reports, the number of correspondent banks fell by 25% between 2011 and 2020, further reducing access to the global financial system. This has led to increased costs and frictions in cross-border payments, painting a crucial issue, as remittances often play a more significant role in these economies than development assistance.

Source: World Migration Report

Faced with these barriers, many individuals and businesses are seeking alternative and stablecoins offer a promising solution. By providing a more efficient, cost-effective, and stable means of transferring money, stablecoins can help bridge the gap left by traditional banking systems. In doing so, they offer a pathway to greater financial inclusion, broader access to essential services, and the potential for economic growth and stability in emerging markets.

Center Bank Digital Currency

While private stablecoins have led the charge in the digital currency revolution, central banks around the world are not standing passively by. The rise of stablecoins has caused many central banks to explore the development of Central Bank Digital Currencies (CBDCs), which represent a digital form of a country’s sovereign currency.

Unlike private stablecoins, which are typically issued by corporations or decentralised organisations, CBDCs would be issued directly by central banks, giving them the full backing and credibility of the government, just as their respective fiat currency. This has important implications for the global financial system, as CBDCs could fundamentally alter the way money is issued, transferred, and managed.

China has been the most proactive in this regard, with its digital yuan, known as the e-CNY, already in advanced stages of development and testing. The People’s Bank of China (PBOC) has conducted extensive trials across multiple cities, with millions of yuan in digital currency distributed to citizens and businesses.

The digital yuan is designed to work seamlessly with existing financial infrastructure while also enabling direct peer-to-peer transactions without the need for intermediaries. This could significantly reduce transaction costs and increase the efficiency of payments, particularly in a country like China, where mobile payments are already deeply integrated into daily life.

The implications of the digital yuan extend beyond China’s borders. If widely adopted, the e-CNY could challenge the dominance of the US dollar in international trade and finance, particularly in regions where China has strong economic ties, such as Africa and Southeast Asia.

The digital yuan could also provide a way for countries to bypass the SWIFT system, which is currently dominated by the US, thereby reducing their exposure to US financial sanctions. This geopolitical dimension of CBDCs adds an additional layer of complexity to their development and adoption, as they could become tools of economic influence in the hands of states.

In Europe, the European Central Bank (ECB) is also exploring the issuance of a digital euro. The ECB has launched a two-year investigation phase to assess the feasibility and implications of a digital euro, which would be designed to complement, and not replace existing cash. The digital euro aims to provide a secure and efficient means of payment within the Eurozone, particularly in a digital economy that is increasingly driven by online commerce and mobile payments. The ECB is also considering how the digital euro could enhance financial inclusion, by providing easy access to digital payments for citizens who do not have bank accounts.

The United States, meanwhile, is taking a more cautious approach. The Federal Reserve has published several discussion papers exploring the potential benefits and risks of a digital dollar but has not yet committed to issuing one. The key concerns include the impact on the banking system, as a digital dollar could potentially reduce the demand for bank deposits, which are a primary source of funding for commercial banks. With the election approaching, there are divergent thought between both candidates, with Trump promising to never allow the creation of such currency, whereas ex-candidate President Biden was a strong believer in the benefits of a US-CBDC during his re-election campaign.

However, CBDCs also raise concerns about privacy and surveillance, as governments could theoretically track every transaction made with digital currency. Additionally, the implementation of CBDCs could disrupt traditional banking systems, potentially reducing the demand for commercial bank deposits and altering the way financial institutions operate. This shift could lead to broader economic implications, such as changes in credit availability and interest rates, creating a need for careful consideration of how these digital currencies are integrated into the existing financial landscape.

Disclaimer

This marketing document has been issued by Bank Syz Ltd. It is not intended for distribution to, publication, provision or use by individuals or legal entities that are citizens of or reside in a state, country or jurisdiction in which applicable laws and regulations prohibit its distribution, publication, provision or use. It is not directed to any person or entity to whom it would be illegal to send such marketing material. This document is intended for informational purposes only and should not be construed as an offer, solicitation or recommendation for the subscription, purchase, sale or safekeeping of any security or financial instrument or for the engagement in any other transaction, as the provision of any investment advice or service, or as a contractual document. Nothing in this document constitutes an investment, legal, tax or accounting advice or a representation that any investment or strategy is suitable or appropriate for an investor’s particular and individual circumstances, nor does it constitute a personalized investment advice for any investor. This document reflects the information, opinions and comments of Bank Syz Ltd. as of the date of its publication, which are subject to change without notice. The opinions and comments of the authors in this document reflect their current views and may not coincide with those of other Syz Group entities or third parties, which may have reached different conclusions. The market valuations, terms and calculations contained herein are estimates only. The information provided comes from sources deemed reliable, but Bank Syz Ltd. does not guarantee its completeness, accuracy, reliability and actuality. Past performance gives no indication of nor guarantees current or future results. Bank Syz Ltd. accepts no liability for any loss arising from the use of this document.

#Investors #Betting #Big #Stablecoins #CBDCs