{kind=link}

Why ‘High’ Fees Could Pay Off When You Buy These 8%+ Dividends

When choosing between closed-end funds (CEFs), you might be tempted to put a lot of focus on fees. That makes sense. Nobody likes high costs eating into their returns.

But there’s more to CEF performance than just the expense ratio, and if you focus on buying the funds with the lowest fees, you might leave a lot of money on the table.

Because the truth is, there’s no clear relationship between fees and long-term returns. A CEF’s portfolio and the skill of its managers play a far greater role in determining its success than fees alone.

Breaking Down the Data: No Simple Relationship Between Fees and Returns

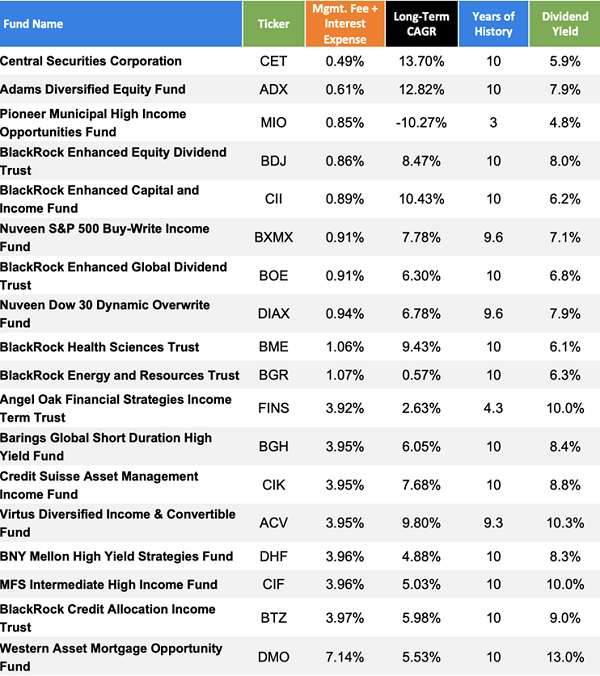

Let’s start with the data. I’ve collected information on total fund fees for CEFs with some of the highest and lowest 10-year compound annual growth rates (CAGRs), or in the case of newer funds, annualized returns since inception. You might expect lower fees to lead to higher returns, but the numbers say something different.

It starts out well for the low-fee funds: Central Securities Corporation (NYSE:), with the lowest combined management fee and interest expense on our list, just 0.49%, boasts an impressive 10-year CAGR of 13.7%—the highest on our list—as of this writing.

The return on our second-cheapest fund by fees, the Adams Diversified Equity Fund, Inc (NYSE:), a long-time holding in our CEF Insider service, also looks like a win for low-fee investing, with a fee of 0.61% and a solid 10-year CAGR of 12.82%.

But the connection falls apart after that.

The third-cheapest fund by fees above, the Pioneer Municipal High Income Opportunities Fund, Inc. (MIO), offers a low expense ratio of just 0.85% but a devastating long-term CAGR of -10.27%.

Meantime, the expensive (on a fee basis) Virtus Diversified Income & Convertible Fund (NYSE:), with nearly 4% fees, has a strong 9.8% CAGR and outruns several funds offering lower fees.

Clearly, just because a fund offers low fees doesn’t mean it’s a winner. A fund’s success depends much more often on how well its portfolio is managed than how low its fees are.

To be sure, skilled managers who can navigate the markets effectively may justify their fees by delivering superior performance. The BlackRock Health Sciences Trust (NYSE:) is a good example: Its fees are 1.06%, but it posted a 9.4% CAGR over the last decade, beating many lower-fee funds.

The Real Drivers of CEF Gains: The Portfolio and Management Skill

Meanwhile, funds like the Credit Suisse Asset Management Income Fund Inc. (NYSE:) and Barings Global Short Duration High Yield Fund (NYSE:), which charge still-pretty-hefty fees of around 4% each, have delivered solid returns for a while now.

Strong Returns Despite High Fees

This success is due to strong management and smart portfolio positioning, not their fee structure.

The Takeaway: Don’t Get Hung Up on Fees

It’s tempting to focus on fees as the make-or-break factor when choosing a CEF. After all, index funds have conditioned us to believe that lower costs equal better performance.

But CEFs are different. They offer access to unique strategies, leverage and most importantly liquidity in the form of high dividends: The top-performing funds on our list above offer yields around 8%.

You just can’t get that kind of cash flow—and the financial independence it provides—from index funds. And getting that kind of cash flow out of any portfolio requires active management.

So while fees matter, they’re not the end of the conversation. We need to dig deeper and evaluate management’s skill and portfolio. Funds with higher fees may still deliver strong returns if they’re in the hands of a capable manager navigating the right sectors. On the other hand, low-fee funds can still be losers if the portfolio is poorly positioned.

Urgent: 5 CRITICAL Monthly Dividends to Buy (Yielding 10.5%+) as Rates Fall

Over the last few days, I’ve been urging investors to pick up 5 monthly dividend funds kicking out a rich 10.5% average dividend.

These are my “best of the best” buys as rates drop, sending income-starved investors on the hunt for higher yields. They’re cheap now, but that won’t last. My forecast: 20%+ price gains from each of them 12 months from now, and that’s in addition to their rich 10.5% dividends (paid monthly!).

Disclosure: Brett Owens and Michael Foster are contrarian income investors who look for undervalued stocks/funds across the U.S. markets. Click here to learn how to profit from their strategies in the latest report, “7 Great Dividend Growth Stocks for a Secure Retirement.”

#High #Fees #Pay #Buy #Dividends