{kind=link}

Cisco on the Brink: Is a Resurgence for Old Tech in Sight With Upcoming Earnings?

Cisco (NASDAQ:) reports its fiscal Q1 2025 financial results after the closing bell on Wednesday, November 13 2024, with analyst consensus estimates expecting the following:

- Revenue: $13.77 billion, for -6% y-o-y growth

- Operating income: $4.5 billion, for -16% y-o-y growth

- EPS: $0.87 per share, for -22% y-o-y growth

While this might look pretty grim to readers, the fact is that this fiscal Q1 ’25 is the last tough “compare” Cisco has against last year’s “inventory overhang” the forward estimates are looking for better growth from the networking giant.

In fiscal Q4 ’24, Cisco guided to a mid-point of $13.75 billion, but the actual consensus estimate is a little bit higher coming into the Wednesday night release.

In terms of “forward, expected growth” here’s how the next 3 fiscal years annual estimates look for the 1990’s telco networking stalwart:

- 2027 EPS growth: +8% expected

- 2026 EPS growth: +9% expected

- 2025 EPS growth -4% expected

- 2027 rev growth: +4% expected

- 2026 rev growth: +5% expected

- 2025 rev growth: +1% expected

For a stock trading at 15x – 16x EPS, that is expected to “average” 3% revenue growth and 4% EPS growth over the next 3 years, the most compelling investment case you can make for the stock is that it’s NOT a mega-cap 7 name, and there are such low expectations around Cisco, it becomes a “it’s so bad, it’s good” scenario.

Again, the stock’s valuation at 15x forward EPS of 4% expected EPS growth, 3x revenue, and 17x and 24x price-to-cash-flow and price-to-free-cash-flow doesn’t really leave any one very excited.

From a longer-term perspective, Cisco has tried for 25 years to reinvent themselves after the dot.com bust, but regardless of how many times Cisco tried to restructure the segments and put a fresh face on the business, the legacy telco networking business of switches and routers still being about half the business (from what I can tell) is like swimming an ironman towing an aircraft carrier around the pylons.

The numerous smaller acquisitions never worked, or seemed to work in terms of adding accretive revenue growth, and in fact Cisco’s acquisition strategy seemed to do nothing but dilute shareholders for the last 25 years.

The Splunk (NASDAQ:) acquisition looks more interesting, but in fiscal Q4 2024 (according to a note out of Jefferies and Morningstar), Splunk was below the midpoint of the revenue guidance ($960 million in revenue vs the $975 million estimate) which may not be a good sign this early into the integration.

Cisco did cross $1 billion in cumulative AI orders for Cisco, which the Jeffries analyst seemed mildly positive about.

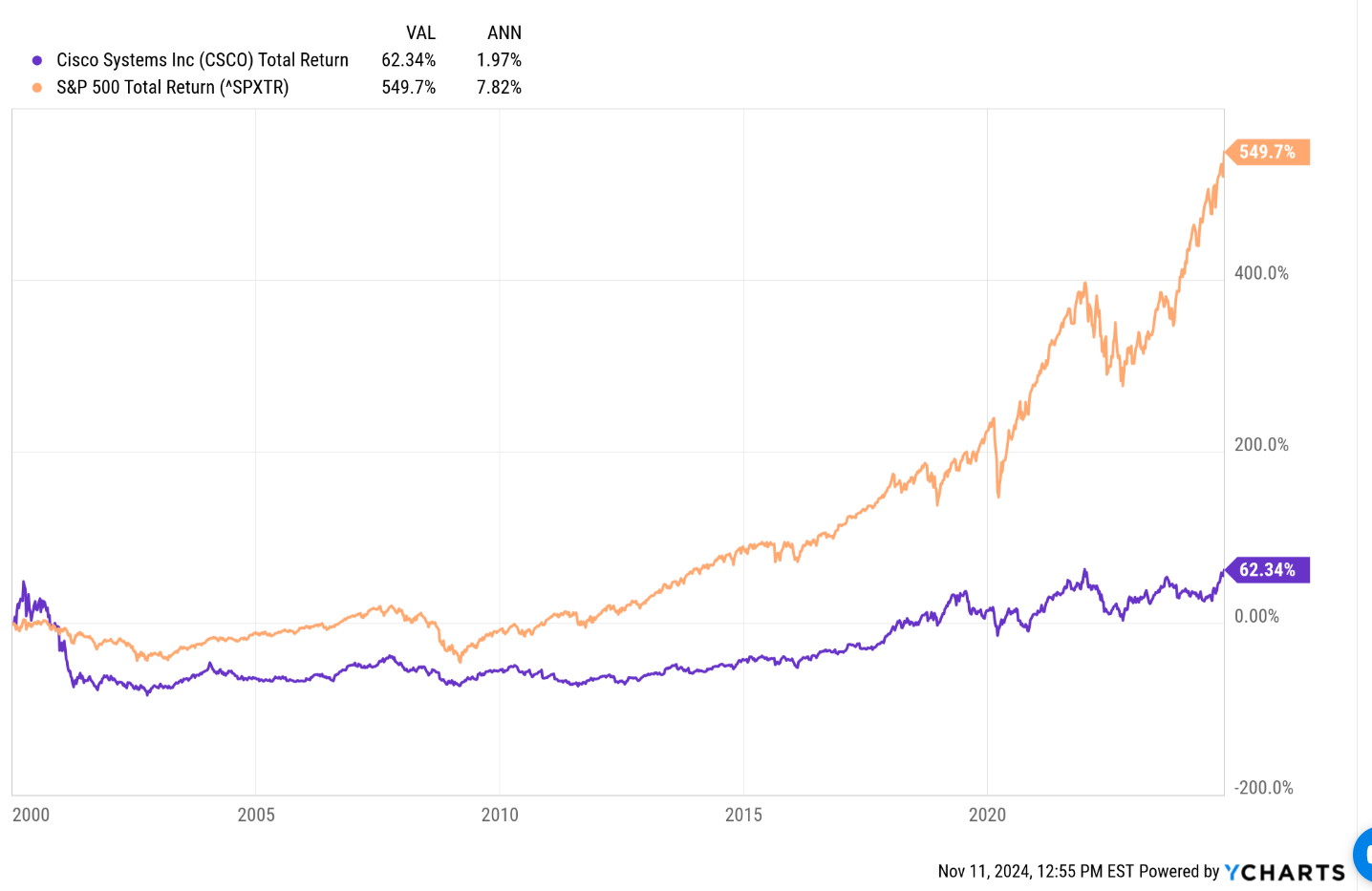

Performance vs S&P 500:

If you are wondering how Cisco has performed the last 25 years, here’s a comparison with the :

Those performance numbers are quite grim.

Cisco has averaged a 2% annual return for 25 years.

It should also not be lost on the “AI and the mega-cap 8 crowd” of today.

Conclusion

If readers are looking for some compelling case to own Cisco at this point in time, one can’t be made, other than the stock is completely uncorrelated to the ’s bull market over the last 15 – 17 years, or since the March 9, 2009 generational lows for the S&P 500, as the performance chart indicates.

Cisco could very well find a bid in a market that really trashes the mega-cap 7 or 8, if only from “there are few other tech stocks to own” in a market that might resemble 2001 and 2002, when the fell 80%, which I wouldn’t expect today.

This blog has owned Cisco in the past for clients, as a smaller, non-growth, tech position, but the problem is it chronically underperforms the S&P 500, and what made it worse, and the reason the stock was eventually sold, was that after underperforming the S&P 500 in the post-Covid era, March, 2000 through late 2001, management guided down around May, 2022, so it underperformed in a down market too.

That hurts. I don’t think it’s unreasonable for a portfolio manager to expect stocks that underperform in bull markets, to hold or maintain some relative value in down markets, since they are not the proverbial “crowded trades”.

Cisco hasn’t done that.

Tech transitions like the AI initiative, and the tremendous spending it generates can be opportunities for companies – particularly tech companies – to reinvent themselves, but software is much easier than hardware. Cisco’s Security business never seemed to gain traction, nor did it’s software initiatives.

Look at Intel (NASDAQ:).

We’ll see if Splunk can make a material difference towards revenue growth and or margins.

Don’t worry about trying to pick bottoms: given that long-term performance chart, investors will likely have plenty of time to get on board if Cisco starts to generate some meaningful revenue growth or margin improvement.

Disclaimer: None of this is advice or a recommendation, but only an opinion. Past performance is no guarantee of future results. Investing can and does involve the loss of principal even for short periods of time.

#Cisco #Brink #Resurgence #Tech #Sight #Upcoming #Earnings