{kind=link}

This Popular ETF (and These 6 Stocks) Are Set to Lose in Trump 2.0

We are drowning in post-election stock-market predictions, so let me go ahead and throw another one on the pile:

This new administration will hurt the returns of folks who simply buy an index fund like the (SPY) and call it a day.

I call SPY “America’s ticker” because, well, most Americans own it. If you’re reading this, there’s a good chance you do, too.

Now, I’m not going to judge (well, maybe I will, but just a little bit!).

Suffice it to say, the coming presidential term will usher in a true stock picker’s market—a time when prudent moves into, and out of, individual dividend payers will be key.

That puts holders of SPY, which has to represent the current makeup of the , in a tough spot. Since it has no manager who can buy and sell as markets shift (a big reason why we prefer actively managed CEFs over ETFs), SPY holders are locked in as losing stocks cancel out some or all of the ETF’s winners.

It’s already happening.

Let’s run through six tickers worth pruning from your portfolio before the new administration is sworn in (in addition to SPY, of course!).

Food and Drug Stocks to Fade as We Move Into Trump 2.0

Let’s start with RFK Jr., President-elect Trump’s choice to head the Health and Human Services department. The appointment—should it be confirmed by the Senate—is a clear negative for two corners of the market: food stocks and drug makers.

RFK has been a vocal critic of the pharma industry. He wants alternative therapies and treatments, which are not patentable by drugmakers. He’s also looking to revise how clinical trials are conducted and is targeting lower drug pricing—good for consumers, not so much for pharma profits. And finally, he’s been a sharp critic of processed foods, including artificial coloring used in breakfast cereals and other snacks.

That puts vaccine maker Moderna (NASDAQ:) near the top of our “avoid” list, as well as big-food stocks like General Mills (NYSE:) and The Kraft-Heinz Co. (NASDAQ:), a company we’ve long criticized for being out of step with the times, and fast-food makers like McDonald’s (NYSE:).

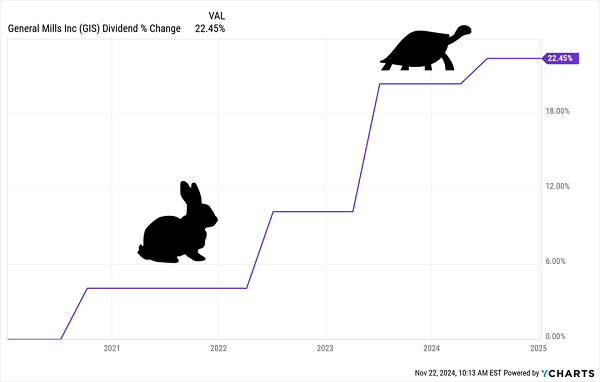

Since we’re investing for dividend growth, we’ve naturally avoided these four. MRNA, for its part, yields 0% today, while General Mills’ payout growth has dropped sharply, rising by just a penny last year:

General Mills’ Dividend Was Decelerating Before the Election

McDonald’s, of course, is still recovering from its E. coli outbreak, plus it pays a high 73% of free cash flow (FCF) as dividends, well over my 50% “safety line.” That’s another brake on future payout growth.

KHC? Its 5.2% dividend yield might grab your attention, but that high yield only exists because the stock has plunged 59% in the last decade (and share prices and dividend yields move in opposite directions).

The last move KHC’s dividend made was actually a cut announced in early 2019, which took the share price down with it. That’s proof positive that our Dividend Magnet—or the tendency for dividend growth to propel share prices higher—also works in reverse:

KHC’s “Reverse Dividend Magnet” Sinks Its Stock

Throw in revenue growth that’s gone nowhere for the better part of a decade and a dividend that accounts for a high 65% of KHC’s last 12 months of FCF, and the chances of this payout getting off the mat, and giving the share price a lift, are slim.

This is a good spot to wheel back on SPY because, yes, all four of the stocks we’ve talked about so far are held by “America’s ticker.” And they’re far from alone on our sell list. Beyond food and drug stocks, there’s another category of S&P 500 dividend payers we want to avoid in the months ahead: those with a lot of China exposure.

China Tariffs No Fun for These 2 Toymakers

Look, I know there’s a debate as to whether the president-elect’s tariff talk is a real threat or a way to bring other countries to the negotiating table. But the smart money says we’ll almost certainly see more tariffs on Chinese exports to the US.

Economists polled by Reuters see a 40% tariff, short of the 60% Trump has called for. But of course, that (like all predictions) should be taken with a grain of salt.

But it is fair to say that companies that still source a lot of product from China will likely take a hit. Two I’m particularly worried about are toymakers Mattel (NASDAQ:) and Hasbro (NASDAQ:).

This duo aren’t only at risk due to higher tariffs. Demographic changes are also an overhang, with people having fewer children, especially in wealthier countries. In 2023, for example, there were just under 3.6 million births in the US, according to the Centers for Disease Control and Prevention, the fewest since 1979.

To be clear, I should say that both companies deserve credit for their efforts to shift production away from China. Mattel recently said it’s closing a plant in the country. And in its first-quarter earnings call, CEO Ynon Kreiz said the firm now gets about 50% of its products from China, though he says that number is falling.

As for Hasbro, according to the WSJ, it gets around 40% of its products from China, with the goal of cutting that to 20% in the next four years. That’s still a heavy reliance, and you and I both know that relocating big parts of a supply chain isn’t something that happens overnight.

Moreover, Hasbro gets most of its sales (67% in Q3) from its consumer-products segment, home of its physical toys and games—even as more kids get their fix online.

You can see the results in the company’s third-quarter revenue, which fell 9%, excluding the sale of its eOne movie and TV business. That was directly tied to a 10% drop in consumer-products sales.

The dividend? Sure, it yields a decent 4.5% today, but it’s gone nowhere since before the pandemic:

Hasbro’s Payout Growth Goes Flat

Mattel, for its part, is off our list for the same reason as Moderna: It doesn’t pay a dividend, having suspended its payout in 2017.

The bottom line is that the winds have shifted against these two, and there’s no sign of that changing anytime soon. Further China sanctions will only weigh on their stocks—and by extension the returns of our SPY holders.

The Dividend Magnet: Our Roadmap for Trump 2.0

There’s one “truth” we can count on as we move into the next Trump administration: A stock’s dividend growth is—and will always be—the No. 1 driver of its share price.

That makes our Trump 2.0 strategy simple: Buy stocks with payouts that aren’t only growing but accelerating—and make sure these companies have the rising sales, earnings and cash flow to keep that growth coming.

Even better if we can grab stocks whose share prices “lag” their payout growth. Then we can ride along as those stocks “snap back” to their dividends.

This is easier said than done, of course: To track dividend/share price correlations, we need complex charting tools and a lot of time to pore over annual and quarterly earnings reports.

But not to worry: I’ve done the legwork for you here. The result is my 5 top “Dividend Magnet” picks, which I’m urging all investors to consider right now.

These 5 stocks have what it takes to keep their share prices—and payouts—popping no matter who’s in the White House.

Disclosure: Brett Owens and Michael Foster are contrarian income investors who look for undervalued stocks/funds across the U.S. markets. Click here to learn how to profit from their strategies in the latest report, “7 Great Dividend Growth Stocks for a Secure Retirement.”

#Popular #ETF #Stocks #Set #Lose #Trump