{kind=link}

2 Stocks With Nearly 20% Downside Risk to Avoid at All Costs

- Cracks are starting to emerge in the year-to-date rally on Wall Street amid uncertainty over the Fed’s rate cut outlook.

- Using the InvestingPro Stock Screener, I searched for overvalued stocks with significant downside risks as per InvestingPro’s ‘Fair Value’ models.

- In this article, we will take a look at three stocks with the highest downside risk based on insights from InvestingPro.

Investors navigating the market landscape often seek opportunities for substantial gains. However, recognizing potential pitfalls and identifying stocks to steer clear of can be just as important for safeguarding one’s portfolio.

In this regard, our predictive AI stock-picking tool can prove a game-changer. For less than $9 a month, it will update you on a monthly basis with a timely selection of AI-picked buys and sells, giving you a significant edge over the market.

Subscribe now and position your portfolio one step ahead of everyone else!

Another fantastic option — also included in the InvestingPro subscription — is to assemble a shortlist of overvalued stocks with significant downside risks using the InvestingPro Stock Screener.

By utilizing this tool, investors can filter through a vast universe of stocks based on specific criteria and parameters, saving them substantial time and effort. Let’s dig in.

How to Avoid Losers

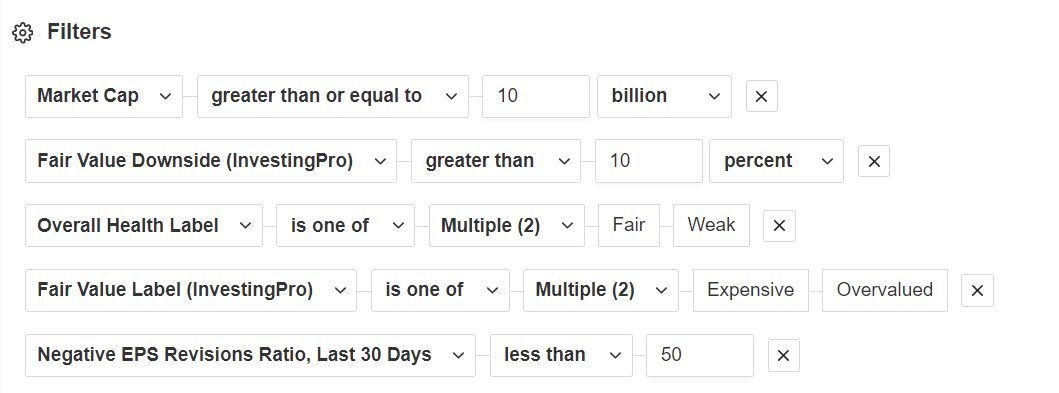

In order to find the companies investors should avoid at all costs, I first scanned for stocks with a market cap greater than or equal to $10 billion and that have InvestingPro ‘Fair Value’ downside greater than 10%.

I then filtered for companies that also possess an Overall Health Label of either ‘Fair’ or ‘Weak’ and that have suffered over 50% negative EPS revisions in the last 30 days.

Source: InvestingPro

If you’re looking for more actionable trade ideas, I’ll be hosting a free webinar on Monday, April 8 at 8:00AM ET/1200GMT in which we will explore the transformative power of Investing Pro’s Fair Value analysis and decode how to identify optimal buying opportunities in the market.

Enroll here:

In total, the screener flagged 21 companies that met those criteria, as indicated by InvestingPro’s insights.

Source: InvestingPro

With both companies mentioned below facing challenges ranging from weakening earnings prospects to high valuation multiples, investors are advised to exercise caution and consider avoiding these stocks in their investment portfolios.

1. Marvell Technology

- Thursday’s Closing Price: $70.88

- Fair Value Estimate: $59.66 (-15.8% Downside)

- Market Cap: $61.5 Billion

Marvell (NASDAQ:) Technology, a prominent player in the semiconductor industry, has encountered a turbulent ride in the markets this year.

Shares rallied to a 2024 high of $85.76 on March 7, before pulling back by as much as 26% to a low of $63.46 on March 19. MRVL stock ended at $70.88 on Thursday, earning the chipmaker a valuation of $61.5 billion.

Source: Investing.com

Despite initial optimism, Marvell has faced headwinds, grappling with various challenges affecting its overall performance.

The company’s shares have struggled to gain traction amid concerns over weakening demand in its enterprise networking and wireless carrier markets.

Marvell makes networking and data storage chips used in cloud computing, telecommunications, automotive, and other applications.

Indeed, InvestingPro has raised cautionary flags on Marvell, with ProTips pointing out its diminishing earnings prospects and high valuation multiples.

Source: InvestingPro

Marvell is forecast to release its first-quarter financial results next month and results are expected to show a double-digit decline in both profit and sales growth.

Underscoring several near-term headwinds facing the company, all 23 analysts surveyed by InvestingPro have cut their EPS estimates as Wall Street turned bearish on the semiconductor maker.

Source: InvestingPro

Consensus calls for Marvell to deliver earnings per share of $0.24, falling 22.6% from EPS of $0.31 in the year-ago period. Revenue is expected to drop 12.1% year-over-year to $1.16 billion.

InvestingPro’s ‘Fair Value’ price target estimate for Marvell Technology highlights the downside risk, with an implication of a nearly 16% potential decline from its current market value.

Source: InvestingPro

That would bring MRVL closer to its ‘Fair Value’ of $59.66 per share.

2. Dollar Tree

- Thursday’s Closing Price: $129.74

- Fair Value Estimate: $109.35 (-15.7% Downside)

- Market Cap: $28.3 Billion

Similarly, Dollar Tree (NASDAQ:), a renowned retail chain specializing in discount variety stores, has encountered its share of challenges lately, leading to concerns among investors.

DLTR stock ended Thursday’s session at $129.74, not far from a recent year-to-date low of $124.01 reached on March 14.

At current valuations, Dollar Tree has a market cap of $28.3 billion, making it the second largest U.S. dollar store and one of the biggest discount retailers in the country.

Source: Investing.com

The company’s stock performance has been lackluster this year, facing pressure amidst a backdrop of weakening demand for general merchandise and higher-margin items amid the current macro environment.

The retailer is also vulnerable to the negative impact of the ongoing industry-wide trend of retail theft, or ‘shrink’.

It should be noted that InvestingPro has sounded the alarm on Dollar Tree, flagging it as a stock to avoid in light of its deteriorating earnings prospects and high level of operating debt.

Source: InvestingPro

Dollar Tree’s update for the first quarter is scheduled to come out next month and results are expected to take a hit from a decline in customer traffic at its stores as well as higher cost pressures and decreasing operating margins.

Not surprisingly, profit estimates have been revised to the downside 15 times in the past 90 days, according to an InvestingPro survey, compared to zero upward revisions.

Source: InvestingPro

Wall Street sees Dollar Tree earning $1.44 per share in the first three months of 2024, declining about 2% from EPS of $1.47 in the year-ago period. Meanwhile, revenue is anticipated to inch up 4% to $7.65 billion.

InvestingPro’s Fair Value price target estimate for Dollar Tree also suggests a nearly 16% downside potential, underlining the risks associated with the stock.

Source: InvestingPro

That would move DLTR closer to its ‘Fair Value’ set at $109.35 per share.

Be sure to check out InvestingPro to stay in sync with the market trend and what it means for your trading.

Readers of this article enjoy an extra 10% discount on the yearly and bi-yearly plans with the coupon codes PROTIPS2024 (yearly) and PROTIPS20242 (bi-yearly).

Subscribe here and never miss a bull market again!

Disclosure: At the time of writing, I am long on the S&P 500, and the via the SPDR S&P 500 ETF (SPY), and the Invesco QQQ Trust ETF (QQQ). I am also long on the Technology Select Sector SPDR ETF (NYSE:).

I regularly rebalance my portfolio of individual stocks and ETFs based on ongoing risk assessment of both the macroeconomic environment and companies’ financials.

The views discussed in this article are solely the opinion of the author and should not be taken as investment advice.

#Stocks #Downside #Risk #Avoid #Costs