{kind=link}

Better-Than-Expected Bank Results Set the Tone for Q3 Earnings Season

-

Banks kicked off the earnings season with mostly bullish results and commentary.

-

Q3 S&P 500 EPS growth is expected to come in at 4.1%, the fifth consecutive quarter of growth.

-

First of the Magnificent 7 release results next week when Tesla reports.

- Peak weeks for the Q3 season run from October 28 – November 15.

The earnings season started strong with some positive results from the big banks which all blew away analyst estimates. Results mostly impressed investors who responded positively to reports on Friday and Tuesday morning, with the latter eventually overshadowed by an Nvidia (NASDAQ:) sell-off which took markets lower that day. Morgan Stanley got things back on track on Wednesday with impressive results which led the major indices higher.

However, it was earnings results from another sector’s constituent on Thursday that drove markets. Taiwan Semiconductor Manufacturing (NYSE:) saw its stock soar after posting robust profits due to increased AI demand which the company said should continue for “many years.”

As a result, other big AI players such as Nvidia and AMD (NASDAQ:) and to a lesser degree Apple (NASDAQ:) and Microsoft (NASDAQ:), saw their stocks move higher, just ahead of big tech earnings season which kicks off the week of October 28.

One major thesis leading into this earnings season was that lowered sell-side estimates heading into reports would lead to bigger beats and happier investors. That’s more or less what happened with the banks, with some caveats, of course.

Are Banks Getting Flowers?

All six of the big banks beat analysts’ profit expectations, and all but Wells Fargo & Company (NYSE:) surpassed revenue estimates. Most of these names saw their stocks rewarded as a result of better-than-expected results, even WFC’s stock price popped 6% on the day of their earnings report despite missing on the top line. On the flip side, Citigroup Inc (NYSE:) beat both metrics but still saw their stock slide 5% (after initially popping up 1%) as a result of increasing loan loss provisions. Bank of America also reported positive surprises but the stock ended the day flat.

Overall the takeaways from the big banks were bullish.

On the consumer: The story on the health of US consumers remains the same, while spending activity remains intact, consumers remain cautious and credit cards are getting paid off at a slower rate than usual.5 Lower rates have encouraged more borrowing, but real estate hasn’t quite seen the relief expected.

Investment banking: The investment banks (specifically, Goldman Sachs6 and Morgan Stanley7) performed well in Q3 due to an increase in fees and increased activity specifically in M&A. With the Federal Reserve implementing a jumbo rate cut last month and expected to continue cutting interest rates at the next several meetings, that should make borrowing money more enticing and therefore increase the deal pipeline.

Trading: Equities trading revenues boosted all of the big bank’s bottom lines, while FICC trading came in lower, and in some cases, negative on a YoY basis.

Overall: The soft landing is here according to JPMorgan, with CFO Jeremy Barnum commenting “these results are consistent with a soft landing” on their conference call8, and similar sentiment was indicated by their peers as well.

Q3 Earnings Scorecard

For the Q3 season, S&P 500 EPS growth is expected to hit 4.1%, which would be the fifth consecutive quarter of bottom-line growth. Note that 4.1% is a blended growth rate that includes results for those companies that reported as of Friday, October 11 and estimates for those that have yet to report. Revenues are expected to come in even higher with 4.6% YoY growth.

On a sector level, Information Technology, Communication Services, and Health Care all remain leaders on the top and bottom line, while Energy is the only sector expected to post YoY declines on both metrics.

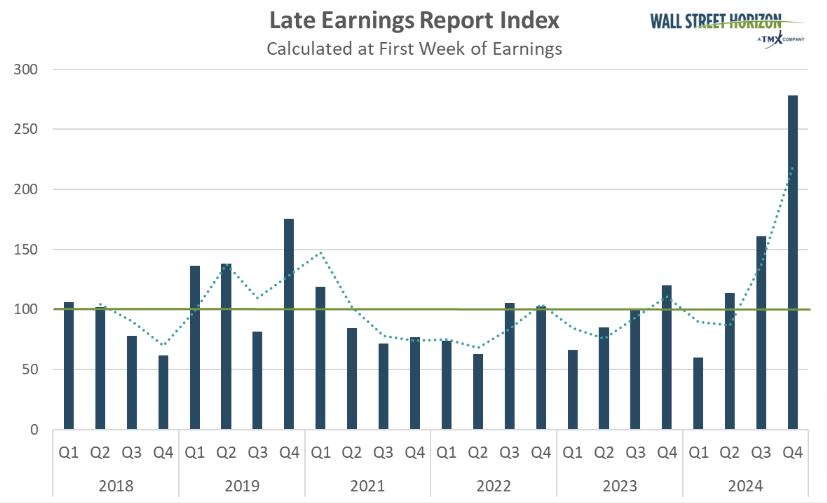

More Companies Pushing Back Q3 Earnings Dates – Likely Due to Upcoming US Presidential Election

After falling to its lowest level in its nine years in the first quarter of 2024, the Late Earnings Report Index, our proprietary measure of CEO uncertainty, has been higher for the last two quarters.

The LERI tracks outlier earnings date changes among publicly traded companies with market capitalizations of $250M and higher. The LERI has a baseline reading of 100, and anything above that indicates that companies are feeling uncertain about their current and short-term prospects. A LERI reading under 100 suggests that companies feel they have a pretty good crystal ball for the near term.

The official pre-peak season LERI reading for Q3 (data collected in Q4) stands at 278, well above the baseline reading. Typically, this would suggest that companies are feeling less certain about economic conditions, but this quarter we believe there is another culprit.

On November 5, the US will elect its next president, and that week is typically a peak one for the Q3 season. Many companies that would usually report that week have pushed off their announcement to the following two weeks to avoid getting lost in the election coverage. As of October 11, there were 105 late outliers and 34 early outliers.

On Deck Next Week

Next week is not quite peak season yet, but contains some highly watched earnings reports. Results from the Magnificent 7 will start to trickle in when Tesla (NASDAQ:) reports on Wednesday. We’ll also get a read on the Industrials sector next week when 3M, Texas Instruments (NASDAQ:) and Honeywell (NASDAQ:) report. Expectations for Industrials remain low with profits only expected to grow 1% YoY and revenue growth estimates at 0.1%.

Q3 Earnings Wave

This earnings season, the peak weeks will fall between October 28 – November 15, with each week expected to see over 2,000 reports. Currently, November 7 is predicted to be the most active day with 1,475 companies anticipated to report.

Thus far, only 59% of companies have confirmed their earnings date (out of our universe of 11,000+ global names), so this is subject to change. The remaining dates are estimated based on historical reporting data.

#BetterThanExpected #Bank #Results #Set #Tone #Earnings #Season