{kind=link}

Deciphering India’s Internet Stocks with Their Fair Values

Goldman Sachs (NYSE:) recently provided an insightful analysis of the performance and prospects of key companies within the Indian internet sector. Let’s break down the key points highlighted in their report

Zomato (NS:) (Buy; 25% Upside)

Goldman Sachs predicts rapid revenue growth of approximately 61% year-on-year for Zomato in the fourth quarter of fiscal year 2024, significantly outpacing the sector average of around 25% year-on-year. They also foresee substantial margin expansion of about 190 basis points quarter-on-quarter in the same period.

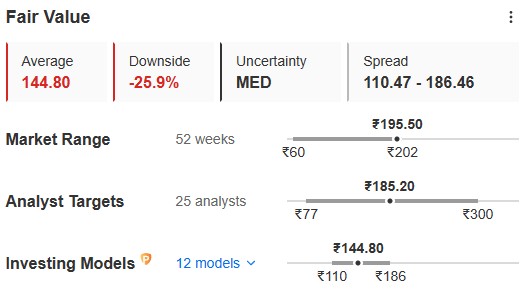

Image Source: InvestingPro+

The firm is bullish on Zomato’s potential, particularly highlighting the quick commerce segment, where they project revenues to exceed consensus estimates for fiscal years 2025 and 2026. Despite Zomato’s significant growth, Goldman Sachs believes the stock remains attractively valued compared to peers, attributing this to its growth and margin visibility, with potential upside to street estimates.

InvestingPro values the stock at INR 144.8 per share.

MakeMyTrip (Buy; 17% Upside)

Goldman Sachs raises its earnings before interest, taxes, depreciation, and amortization (EBITDA) estimates for MakeMyTrip by up to 5%, alongside increasing the target price to US$84 from US$61. They expect robust revenue growth of 23% year-on-year for MakeMyTrip in the fourth quarter of fiscal year 2024, with a stable competitive environment in India’s online travel sector.

Image Source: InvestingPro+

Goldman Sachs also forecasts a significant improvement in MakeMyTrip’s margin profile, driven by ongoing shifts to online platforms and share gains. They believe the market undervalues MakeMyTrip’s potential for sustained revenue growth and anticipate multiples to remain elevated due to high growth visibility.

InvestingPro values the stock at US$ 59.75 per share.

By combining sophistication with flexibility, InvestingPro empowers investors to unlock hidden investment opportunities and navigate the complexities of the stock market with confidence. This ultimate stock analysis tool is now within reach at a discount of up to 69%, offering unparalleled insights for just INR 216 per month, but hurry, this offer won’t last long! Click here to grab your offer

Nykaa (NS:) (Neutral; 18% Downside)

Goldman Sachs maintains a neutral rating on Nykaa, with a target price of INR 140. They anticipate an acceleration in revenue growth for Nykaa’s beauty, personal care, and fashion verticals in the fourth quarter of fiscal year 2024, driven primarily by the beauty and personal care segment.

Image Source: InvestingPro+

However, uncertainties persist regarding Nykaa’s path to profitability, particularly in the fashion and business-to-business sectors. Despite Nykaa’s strong revenue growth projections for fiscal years 2024 to 2026, Goldman Sachs believes the current valuations already reflect this growth potential, with Nykaa trading at a relatively high price-to-earnings ratio of 111x for fiscal year 2026.

InvestingPro values the stock at INR 176.7 per share.

Paytm (NS:) (Neutral; 26% Upside)

Goldman Sachs revises their estimates for Paytm and lowers the target price to INR 420 from INR 450. They anticipate a significant decline in Paytm’s revenues in the fourth quarter of fiscal year 2024 due to regulatory actions by the Reserve Bank of India impacting Paytm Payments Bank Limited. This is expected to particularly affect Paytm’s lending segment, leading to reduced financial services revenues.

Image Source: InvestingPro+

Despite these challenges, Goldman Sachs forecasts a positive adjusted EBITDA for Paytm in the fourth quarter, albeit at a lower margin compared to the previous quarter. They maintain a neutral rating on Paytm due to the wide range of potential outcomes for its earnings in the near term.

InvestingPro values the stock at INR 454.76 per share.

Info Edge (NS:) (Sell; 11% Downside)

Goldman Sachs makes minor adjustments to their estimates for Info Edge and raises the target price to INR 5,260. They expect modest revenue growth of 11% year-on-year in the fourth quarter of fiscal year 2024, supported by improved hiring trends in the quarter.

Image Source: InvestingPro+

While EBITDA margins are forecasted to improve, Goldman Sachs maintains a sell rating on Info Edge due to weak near-term revenue growth outlook for the Indian IT sector, which forms a significant portion of the company’s recruitment billings. They highlight a discrepancy between growth prospects and valuations, suggesting potential downside risk for investors.

InvestingPro values the stock at INR 5,347.83 per share.

X (formerly, Twitter) – Aayush Khanna

#Deciphering #Indias #Internet #Stocks #Fair #Values