{kind=link}

Delta Air Lines: 3 Solid Reasons to Buy the Dip Before Recovery

- Delta Air Lines missed top and bottom line estimates for Q3 2024, but much of the shortfall was attributed to the CrowdStrike software outage leading to 7,000 flight cancellations.

- Corporate travel sales grew by 7% YoY, with strength attributed to the technology, media, and banking sectors, as 85% of companies expect to increase their travel spending in 2025.

- Delta expects record fourth-quarter profits as margins are forecast higher at 11% to 13%, up from 9.4% in Q3.

Delta Air Lines Inc. (NYSE:) reported its third quarter 2024 , and shares initially gapped down in reaction to the headline numbers. Investors were disappointed by the earnings-per-share (EPS) miss by 2 cents, reporting $1.50, along with a revenue miss of nearly $700 million. This sets up the potential for a troubling trend is that it’s the second consecutive quarter that Delta missed consensus analyst estimates.

Delta’s cost per average seat mile (CASM) rose 2% YoY, but total operating revenue per seat mile (TRASM) fell 3.6% YoY. Delta’s earnings release initially impacted its peers airlines in the transportation sector, triggering initial sell-offs in shares of United Airlines Holdings (NASDAQ:) and American Airlines Group (NASDAQ:).

DAL shares closed at $50.62 heading into its earnings release. The stock fell to a premarket low of $47.46 the following morning. However, shares were able to find buyers as they lifted the stock to a modest loss of just 1.35% on the day. Dip buyers have the right idea. Here are three compelling reasons to still buy the dip with both hands on Delta Air Lines stock.

1) The Top- and Bottom-Line Miss Was Due to a One-Time CrowdStrike Software Outage

In July of 2024, Delta Air Lines suffered a computer outage stemming from a flawed software update by cybersecurity firm CrowdStrike Holdings Inc. (NASDAQ:). Delta wasn’t the only airline affected.

The disruption also impacted United Airlines and American Airlines, but not as severe as Delta, which had 7,000 flight cancellations over a week. This hit revenues for a $380 million shortfall and bottom line EPS by 45 cents and increased crew-related costs. It also led to lowering its guidance moving forward.

Demand did cool in the quarter, which caused fare prices to dip, as evidenced by the TRASM drop of 3.6% YoY, but 1.1% of that drop was due to the software problem. Backing out the effects of the CrowdStrike outage would have resulted in a strong EPS beat. This is a one-time event providing a pullback opportunity for prudent investors.

2) The Bar Was Raised for the Fourth Quarter, Expecting Record Profits

As supply continues to improve, September experienced positive domestic and transatlantic unit revenue growth. While the highly profitable transatlantic business had a 3% YoY drop in the quarter, trends are improving due to the Paris demand spike from the Olympics. Corporate travel sales rose 7% YoY, which is double-digit growth in the tech, media, and banking sectors. A corporate study indicates that 85% of companies expect to raise their corporate travel spending in 2025.

The rebalancing of supply and demand, the surge in international flights, and the normalization of costs in the fourth quarter of 2024 bodes well for a sharp upswing in profitability after recovering from the software outage that impacted the third quarter.

Delta expects its operating margin to improve from 11% to 13%, up from 9.4% in Q3. Pre-tax profit growth is forecasted to be 30% YoY, and record profits of $1.4 billion are forecast. Delta also announced its summer Transatlantic 2025 schedule, offering over 700 weekly flights to 33 destinations with seven new routes.

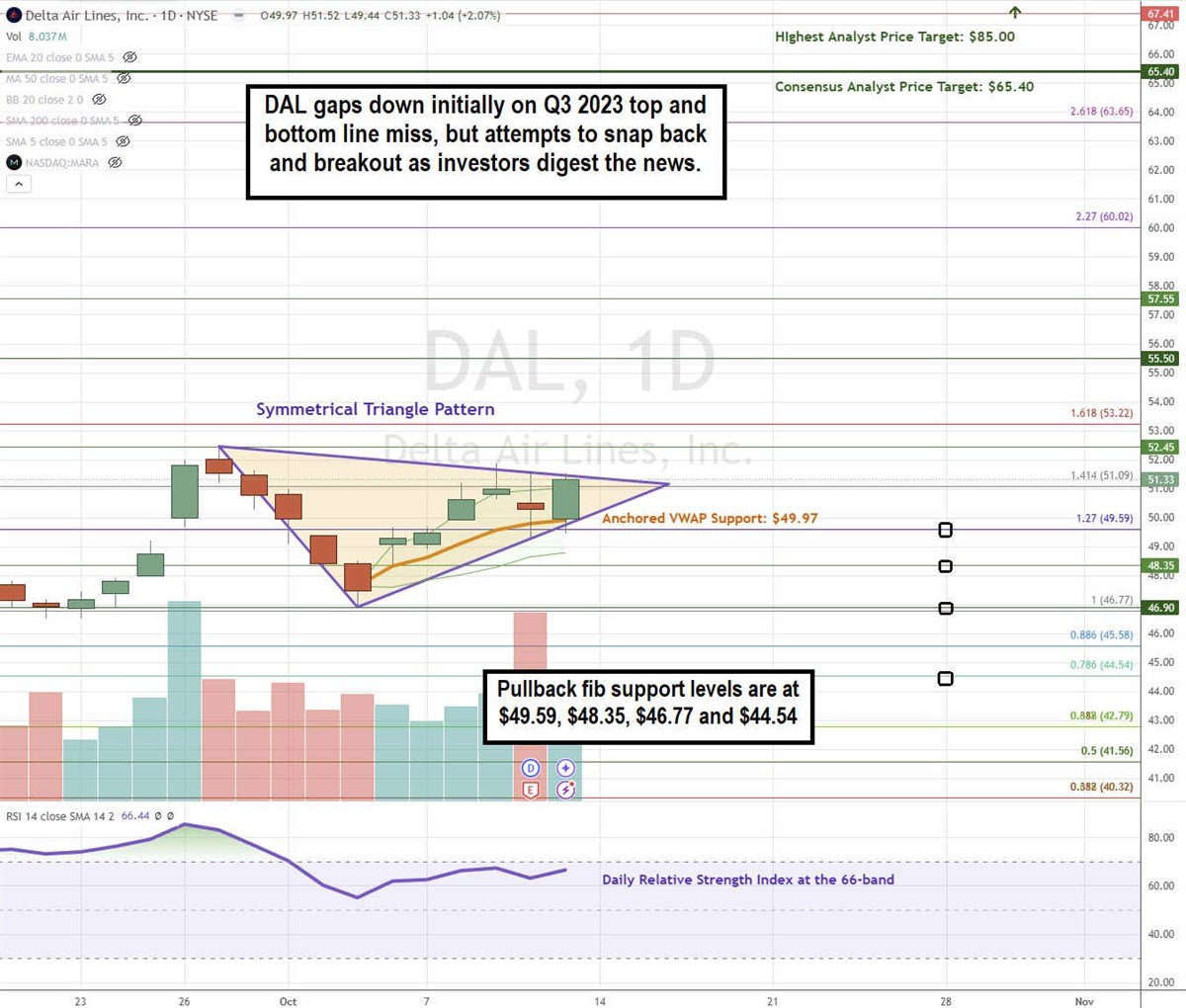

3) DAL Stock Is Forming a Daily Symmetrical Triangle Breakout

A symmetrical triangle is comprised of a descending upper trendline resistance converging with an ascending lower trendline support at the apex point. The breakout occurs when the stock surges through the upper trendline resistance.

DAL formed a swing high at $52.45 on Sept. 27, 2024, before falling to the low of $45.90 on Oct. 3, 2024. These points started the formation of the upper descending trendline resistance and lower ascending trendline support. The lower trendline support held support on the post-earnings gap down, and the upper trendline resistance capped the recovery bounce.

As the channel sets tighter, moving towards the apex, a breakout can trigger if DAL can rise through $52.00. The daily anchored VWAP support is at $49.97. The daily relative strength index (RSI) is rising gradually at the 66-band. Fibonacci (Fib) pullback support levels are at $49.59, $48.35, $46.77, and $44.54.

Delta’s average consensus price target is $65.40, and its highest analyst price target is $85.00.

Actionable Options Strategies: Bullish investors can use cash-secured puts at the Fib pullback support levels to buy the dip. If assigned the shares, writing covered calls at upside Fib levels executes a wheel strategy for income in addition to the hefty 1.17% annual dividend yield.

#Delta #Air #Lines #Solid #Reasons #Buy #Dip #Recovery