{kind=link}

Is the Fed Enough to Save These Beat-Up 7%-16% Yields?

Real estate is great, except for the heavy time commitment, which makes it a non-starter for me.

Enter real estate investment trusts (REITs), which let us invest in not one or two buildings, but usually dozens or even hundreds, for as little as $20 per share or so. Plus the yields can be even better than the fourplex that would ruin my life down the street.

Dividends of 7%, 12% and even 16%. All with a simple ticker that we can tap in from our phones. Now we’re talking. Part of retiring on dividends is never having to field a phone call!

Believe it or not we have Congress to thank. Our fearless lawmakers wrote REITs into existence in 1960. In true D.C. style, they shoved it into an amendment in the Cigar Excise Tax Extension. But we won’t complain about the pork when it is served to us retirees!

The law that brought REITs to life also declared that these businesses would receive a massive federal tax break if they dished big dividends. The loophole? REITs would be tax-advantaged so long as they paid out at least 90% of their taxable income to us, the shareholders.

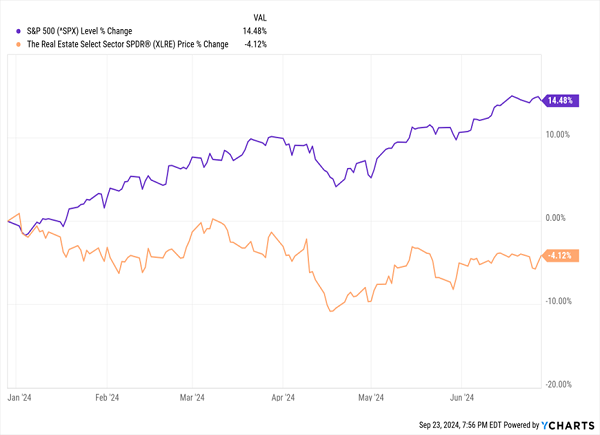

As great as REITs are, however, they don’t go up in a straight line. I pointed out a few months ago that REITs had simply refused to join 2024’s rally, thanks at least in some part to the Federal Reserve refusing to cut rates as quickly as Wall Street expected.

That Was Then

Since then, of course, the economy showed enough signs of cooling that a Fed cut practically became a given—and indeed, in September, our central bank kicked off its cutting cycle with a weighty half-point reduction.

This Is Now

That’s a fantastic turn of events for anyone who used REITs’ prolonged slumber to buy in earlier this year. But I also said:

That’s great news for contrarians who still have some cash to put to work. We want to buy before the Fed finally triggers a stampede in REITs—not after.

So, are we out of time? Are would-be buyers who didn’t pull the trigger doomed to sit on the outside looking in?

Not necessarily.

We need to be a little more discerning, especially where value is concerned—we can’t just blindly throw a dart and hit a bargain like we could a few months ago. And yields in the REIT sector have indeed come down.

But as the following five picks show, we can still lock in phenomenal yields of between 6.9% and 16.2% today.

Let’s start with Armada Hoffler Properties (NYSE:) (AHH, 6.9% yield), the only sub-7% dividend of the group. This diversified REIT owns 73 properties—48 retail, 14 office and 11 multifamily—throughout the Mid-Atlantic and Southeast. But that belies the importance of office to the portfolio. While office real estate makes up just 19% of AHH’s property account, it accounts for 33% of property net operating income (NOI).

So it should be little surprise that this REIT’s shares have been unable to recover to pre-pandemic levels.

Armada Still Isn’t Over COVID

But AHH isn’t entirely unattractive. Armada boasts mid-90s occupancy across all three of its segments. It has been growing same-store cash NOI. The dividend—which Armada admittedly had to hack in half by 2020—only needs to grow by another 7% to return to pre-COVID levels, and it’s decently covered at less than 90% of estimates for adjusted funds from operations (AFFO).

It’s only fairly priced, however, at roughly 13 times those same AFFO estimates. And higher-than-average leverage is expected to weigh on both Armada’s ability to deploy capital, as well as the company’s earnings. It’s not an ideal situation at the moment, but I’ll keep my eye on this one for better opportunities in the future.

Speaking of office properties, let’s move on to Alexanders (NYSE:) (ALX, 7.5% yield), which has one of the sparsest real estate portfolios I’ve ever seen. This hyper-niche office REIT owns a scant five properties in the NYC metropolitan area. It’s also managed by Vornado Realty Trust (NYSE:), which takes annual management fees from several of the properties and is entitled to a development fee, when applicable—money that basically comes out of your pocket.

ALX has also struggled since COVID, but to its credit, it has recently been able to reclaim pre-pandemic levels.

A Little Trouble in the Big Apple

Rather than break down Alexander’s properties, I’ll simply point out that Bloomberg, as a tenant, accounts for a little more than half of rental revenues. Yes, Bloomberg has signed on to remain at 731 Lexington Avenue through 2040, but that’s a worrisome business concentration that should give any investor pause. Indeed, Alexander’s is compelled to warn investors that “if we were to lose Bloomberg as a tenant, or if Bloomberg were to be unable to fulfill its obligations under its lease, it would adversely affect our results of operations and financial condition.”

Alexander’s dividend coverage is also problematic. In 2023, the company’s $15.80 in FFO per share was much less than the $18 per share in dividends it paid out. So far in 2024, it has brought in $8.29 in FFO per share but paid out $9.

I’ve previously highlighted Alexander’s as one of Wall Street’s more hated stocks. The analyst crowd sometimes takes a “if you can’t say something nice, don’t say anything at all” tack with stocks, and that’s the case with ALX, which has a single covering analyst right now. I think I’ll do the same and move on to the next stock.

Easterly Government Properties (NYSE:) (DEA, 7.7% yield) is a refreshing change of pace. OK, yes, this is an office-heavy portfolio, too, but it’s not your average cubicle farm. This REIT owns 93 properties that it leases out to U.S. government agencies such as Veterans Affairs, the FBI, and the Drug Enforcement Administration, among others. And its buildings go beyond offices, spanning outpatient facilities, warehouses, courthouses, labs, even built-to-purpose properties.

Source: Easterly Government Properties August 2024 Investor Presentation

On paper, Easterly is a dividend hunter’s dream. It has one of the best clients you could ask for in the U.S. government. It’s not just diversified by property type, but it has a tenant and property breakdown that no other REIT comes close to replicating. It yields nearly 8%. It’s even trading at a mild discount right now.

Yet for years, DEA shares have given investors little more than heartburn.

But Is Easterly Finally Turning a Corner?

Easterly’s biggest problem is that it hasn’t been able to prove it can grow FFO with any regularity. The government might be a reliable tenant, that it’s also not the best tenant to have for growth purposes. And as I’ve mentioned previously when examining DEA:

Many of its properties are ‘build to suit’—the buildings are exactly what the government needs, but not exactly attractive to outside tenants, either. That means decent bargaining power for the government, and capped upside for Easterly.

The biggest black mark—one that’s almost impossible to ignore—is DEA’s dividend coverage. In a way, the dividend is lucky to have remained flat at 27 cents quarterly since mid-2021. That’s because Q2 marked the seventh straight quarter in which Easterly earned less in cash available for distribution (CAD, a non-GAAP cash flow metric some REITs use to illustrate their ability to cover the dividend) than it paid out in dividends.

That’s not nearly as glaring a dividend problem as the one at Global Net Lease (NYSE:) (GNL, 12.6%).

Global Net Lease is a commercial REIT operator with assets in 11 countries. The U.S. accounts for roughly 80% of straight-line rents, though it also has a presence in Canada and western European nations including the U.K., the Netherlands and Germany. It boasts nearly 1,300 properties leased out to 755 tenants spanning more than 90 industries.

And it pays a double-digit yield despite the fact that management has taken a hatchet to the payout multiple times in recent years.

GNL: 3 Dividend Cuts in 5 Years

I struggle to trust a company with a dividend policy so tight, it’s basically forced to cut back on the distribution anytime management is in a pinch. But there are a few signs of hope that are keeping this stock on my radar.

The big one is that GNL is working to get on more solid financial ground. The company has been selling off assets like crazy (163 properties worth ~$730 million so far in 2024) to bring down its leverage. Midway through the year, net debt to leverage sat at 8.1x. It’s working to get that number as low as 7.4x by the end of this year, and eventually closer to the net-lease industry’s median, which sits below 6.0x. In the meantime, it’s projected to actually grow FFO in each of the next two years.

Plenty must go right for Global Net Lease to right the ship and build trust with dividend investors again. But a still-low P/AFFO of less than 7 right now adds a little curb appeal to this gamble.

Near the end of 2023, I said that patience was a must with Service Properties Trust (NASDAQ:) (SVC, 16.2% yield)—an unusual but intriguing REIT that invests in both hotels and service-focused retail net-lease properties.

I Hope You Listened.

But with shares now trading for just 4 times FFO estimates, is the time finally ripe to hop into this mind-blowing yield?

Service Properties Trust, as I said, has a dual focus: hotels and retail. The former involves some 220 hotels with more than 37,000 guest rooms in the U.S., Canada and Puerto Rico. The latter involves nearly 750 service-focused retail net lease properties in the U.S. And importantly, that retail arm is heavily dependent on TravelCenters (NASDAQ:) of America / Petro Stopping Centers, which make up more than two-thirds of the division’s annualized minimum rent. (The next-closest is The Great Escape at a mere 2%.)

A major drag on SVC has been a massive upgrade project to its Sonestra and Hyatt (NYSE:) hotels; while upgrades will continue throughout 2024, its Hyatt renovations are almost finished, which should provide a tailwind to RevPAR (revenue per available room, a vital hotel performance metric). I also previously mentioned that Service Properties Trust had some $1 billion in debt maturities to address in each of the next two years—it has managed to repay those and now has no debt maturities due until 2026.

Service Properties Trust, like many other REITs, kneecapped its dividend in 2020, from 54 cents per share to a penny. Unlike GNL, SVC has managed to raise it back somewhat, to 20 cents per share. But dividend investors might have cause to be nervous again. The second quarter’s CAD fell from 47 cents per share in 2023 to 29 cents per share in 2024, bringing the REIT’s trailing 12-month CAD to 73 cents per share. Service Properties Trust pays 80 cents annually, meaning the dividend is no longer covered by CAD.

Disclosure: Brett Owens and Michael Foster are contrarian income investors who look for undervalued stocks/funds across the U.S. markets. Click here to learn how to profit from their strategies in the latest report, “7 Great Dividend Growth Stocks for a Secure Retirement.”

#Fed #Save #BeatUp #Yields