{kind=link}

Rocket Lab Is Shaping up to Be a Solid SpaceX Contender

For a long time, it has been accepted that government funding is necessary as a buffer against capital-intensive efforts. One of them is space flight. The success of the Apollo program is difficult to imagine without the government-infused capital for costly development, risky testing, and recovery from failures.

Space Exploration Technologies Corporation (SpaceX) adopted a hybrid public-private partnership approach, representing the next step in pushing these boundaries. Although a private company, it is estimated that Elon Musk’s space venture couldn’t have made it without over $15 billion in government contracts, grants, reimbursements, and subsidies, largely through NASA and the U.S. Air Force.

A step beyond this public-private approach is to have a publicly traded company like Rocket Lab USA, Inc. (NASDAQ:). The question is, should Rocket Lab investors expect the company’s profits to justify the exposure?

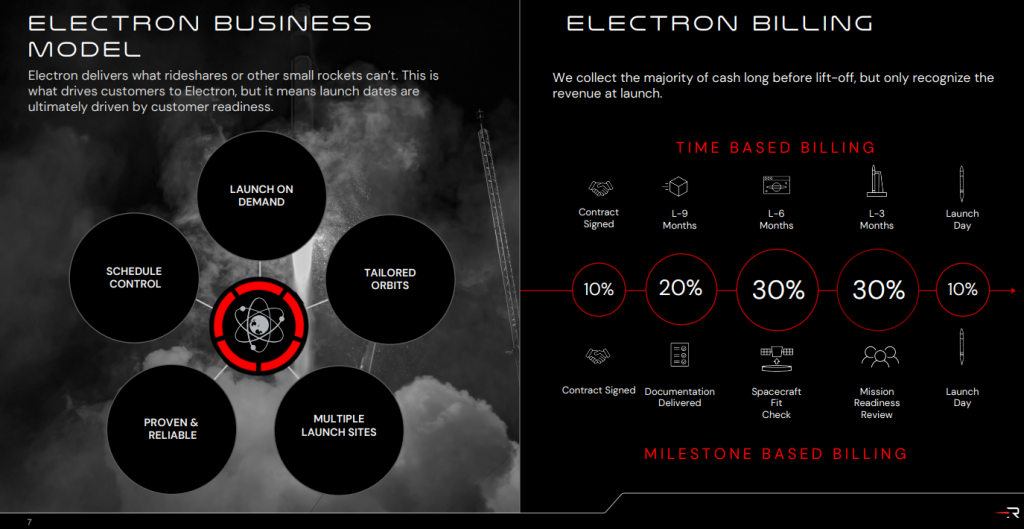

Rocket Lab’s Minimalistic Approach as a Launching Ramp

As engineering solutions and practices are established across the space sector, less risk is involved. In turn, less risk leads to greater financial predictability. Rocket Lab mitigates the capital-intensive nature of space launches with its practical, minimal approach.

Centered around 3D-printed components for its Rutherford engines that streamline production, Rocket Lab also focuses on smaller launches. The company’s Electron rockets can deliver up to 300 kg to low Earth orbit (LEO). Although this is lower than SpaceX Falcon 9’s 22,800 kg capacity, it allows for cheaper and more frequent launches of small satellites.

“Electron remains right-sized for the small sat market, and releasing additional performance is about providing our customers with even more flexibility on the same proven vehicle they have come to rely on.”

Peter Beck, Rocket Lab CEO

Since the first flight in May 2017, Rocket Lab has launched 51 expendable Electron rockets, suffering only four failures and deploying over 190 satellites.

Rocket Lab’s Contracts

After the company’s 10th mission in 2024, building Synspective’s SAR (Synthetic Aperture Radar) constellation, as of August 7th, 2024, Rocket Lab announced its 52nd Electron mission for the US-based Capella Space. The company charged Rocket Lab with a single Acadia-3 SAR satellite for an Earth-imaging constellation.

Previously, in 2021, Rocket Lab secured a U.S. Space Force (USSF) Monolith satellite launch worth $14.49 million. This vote of confidence carried on from 2019’s successful launch of satellites for the STP-27RD mission under the Department of Defence (DoD).

In December 2023, Rocket Lab landed a $515 million contract for 18 Electron launches on the behest of the USSF via the Space Development Agency (SDA) as the largest contract. Carrying on this trend, the government’s aerospace branch, Space Systems Command (SSC), picked Rocket Lab for a $32 million deployment for the VICTUS HAZE Tactically Responsive Space (TacRS) mission.

Set for 2025, the mission will explore the rendezvous and proximity operation (RPO) capabilities of space vehicles. This showcases the company’s reliance on government contracts, having established its wholly-owned subsidiary Rocket Lab National Security for that purpose.

Alongside this steady inflow of government contracts, Rocket Lab also gained the trust of the commercial sector. The most recent one is the 5-rocket launch contract for French company Kineis in June, having charged Rocket Lab to build up a constellation of 25 Kineis satellites for its Internet of Things (IoT) services.

Is Rocket Lab’s Financial Model Working Out?

At a glance, it may seem that Rocket Lab generates its revenue from Electron launches to deploy satellites. However, as of Q2 2024 earnings, Launch Services only accounted for 27.7% ($29.4) of the company’s record-high revenue of $106 million.

The rest of $77 million revenue was owed to the Space Systems division in charge of spacecraft design, component acquisition, mission simulation and control software. This was to be expected following the acquisition of Colorado-based aerospace engineering firm Advanced Solutions, Inc (ASI) in October 2021.

Rocket Lab’s Space Systems was bolstered by its earlier acquisition of Sinclair Interplanetary in April 2020 for its proven satellite hardware tech. Another clever strategy that Rocket Lab employed was the acquisition of solar company SolAero Holdings in January 2022 for $80 million.

While that may seem a high cost for space-grade, radiation-resistant solar cells, it paid off. Namely, the CHIPS Act offset the cost by $23.9 million as of June’s preliminary agreement with the US Department of Commerce.

Overall, Rocket Lab increased its year-over-year revenue by 71%, or 15% quarterly. The company ended the quarter with $1,067 million worth of backlog orders. That said, Rocket Lab is yet to enter the profitability zone, with a reported net loss of $41.6 million, compared to a net loss of $45.9 million in the year-ago quarter.

Nonetheless, the trajectory is moving in the profitability direction owing to the company’s Electron business model.

Given its track record, the company is confident in its next stage—Neutron mid-capacity rockets with up to 13,000 kg payload. This will directly tackle SpaceX’s dominance, as “the medium launch monopoly needs breaking.”

Rocket Lab had already completed the necessary infrastructure for Neutron deployments following the successful tests of the new Archimedes engines. With Neutron on the horizon in 2025, the company expects to tap into a $10 billion total addressable market (TAM) by 2030.

Given its track record, the company is confident in its next stage—Neutron mid-capacity rockets with up to 13,000 kg payload. This will directly tackle SpaceX’s dominance, as “the medium launch monopoly needs breaking.”

Rocket Lab had already completed the necessary infrastructure for Neutron deployments following the successful tests of the new Archimedes engines. With Neutron on the horizon in 2025, the company expects to tap into a $10 billion total addressable market (TAM) by 2030.

Rocket Lab Stock Forecast

Year-to-date, RKLB stock has flatlined at the present price of $5.32. Owing to a positive report, RKLB shares went up 18% over the week. The stock’s 52-week average is $4.65 per share, with a high point of $6.59 and a low point of $3.47.

The high point is well under the RKLB all-time high of $20.72 in September 2021. According to Nasdaq’s forecasting data twelve months ahead, the average RKLB price target is $7.22, which could lead to 35% gains from the current price level.

However, the company could have launch failures in that period. Considering Rocket Lab’s large backlog and future prospects, this would represent another solid “buy the dip” opportunity. The most optimistic outlook puts the RKLB price target at $10 while the less optimistic one is close to current price level, at $4.5 per share.

The bottom line is, RKLB is a borderline penny stock that will certainly exhibit much volatility, but the company is shaping up to be a solid SpaceX contender.

***

Neither the author, Tim Fries, nor this website, The Tokenist, provide financial advice. Please consult our website policy prior to making financial decisions.

#Rocket #Lab #Shaping #Solid #SpaceX #Contender