{kind=link}

S&P 500 Earnings at Record Highs, but Bonds Are Back in the Game

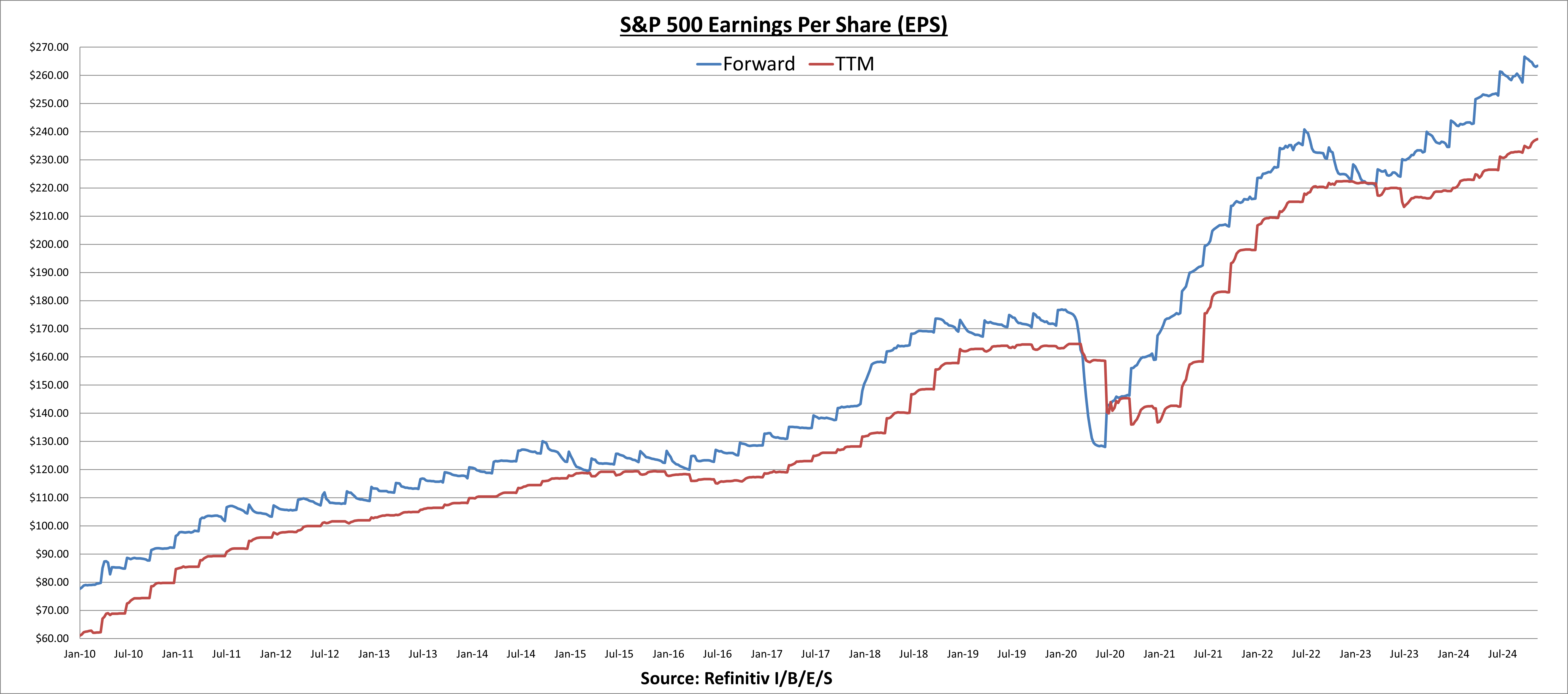

companies have reported a combined $237 in earnings per share over the last 12 months (red line), while the street expects another $263 in EPS over the next 12 months (blue line).

Both at/near all-time times. This represents an expected 11% earnings growth for the S&P 500 over the next 12 months.

95% of S&P 500 companies have now reported Q3 2024 results:

- 76% have beaten street estimates (average 77%)

- Results have come in 7.6% above estimates (average 8.5%)

- Earnings growth rate for Q3 is currently 8.9% (average 11.2)

- Revenue growth rate of Q3 is currently 5.3% (average 6.9%)

Overall the results are slightly lower than recent averages, but still solid. Current estimates are projecting double-digit earnings growth through 2026.

Because of the increase in the price of the S&P 500 index (+26% YTD), the price-to-earnings (PE) ratio has climbed to 22.7, roughly 34% above the 15-year average.

But PE ratios don’t tell the whole story. You have to compare the asset class to alternatives. In this case, fixed income. If we look at the equity risk premium (fancy term for stock valuations compared to treasury bonds), we see that treasuries (blue line) are about as attractive as stocks (red line) for the first time since the 2008 financial crisis.

What this means is that stocks offer little to no margin of safety at current levels. Stocks come with greater volatility compared to bonds, so stock investors want extra compensation for taking on added risks. The fact that valuations between stocks and treasury bonds are about even today, is an advantage for bonds. The PE ratio for the S&P 500 was higher coming out of COVID (around 25), but at that point the treasury interest rate was 1%. So valuations still favored stocks. But now rates have risen above 4%, and for the first time in a long time, fixed-income investors (money markets too) are getting compensated to reduce their risks. This is actually a healthy thing.

Now valuation doesn’t determine the direction of markets (especially in the short term). We saw stocks crash from absurdly high valuations in 2000, and we saw stocks crash again at modest valuations in 2008. What will ultimately determine the future of stock prices is how earnings results come in compared to current expectations, as well as the future path of interest rates. (We’ll discuss this in more detail in future posts – and as we get a better understanding of the economic policies that will come from the new administration.)

Investors are probably fed up with treasuries. They’ve underperformed for a couple of years as rates rose. I’d urge you to consider the purpose of bonds. They are not for growth, they are to help offset the losses during a deflationary bear market. If you’ve ditched your treasury bonds, you now have no protection against the inevitable storm.

If your personal situation calls for 60% stocks and 40% bonds for example, don’t be afraid of bonds. It’s part of being diversified. You’ll always own a piece of something that’s not performing well, and your natural instinct is to want to get rid of it. Please don’t. If your piling into everything that is going up the most, you’ll be sorry when the party is over. It’s not fun or exciting, but it will save you from making some really bad decisions that could threaten your financial goals.

My favorite quote from the movie Wall Street is; “Remember there are no shortcuts son. Quick-buck artists come and go with every bull market, but the steady players make it through the bear markets.” I’m not predicting a bear market here. I’m just saying the best plan of action is to prepare for one before it occurs. Current valuations finally give investors compensation for taking less risk. Take what the market gives you. We can’t predict the future.

#Earnings #Record #Highs #Bonds #Game