{kind=link}

Stocks Week Ahead: Yield Curve Steepening Puts Global Markets on Its Toes

The effects of last week’s market shift are likely to be felt throughout the coming week. The BOJ’s to hike rates and cut back on its bond purchases kicked things off, and the US labor report finished it.

The result was a yield curve that has now broken free of its trading range that has been in place since the summer of 2022, and the is rapidly strengthening across FX pairs.

This has caused the massive unwind of the higher for longer trade, which is the yen carry trade, while the steepening yield curve sends a message of a hard landing in the US, as noted, by rising credit spreads and weaker small-caps.

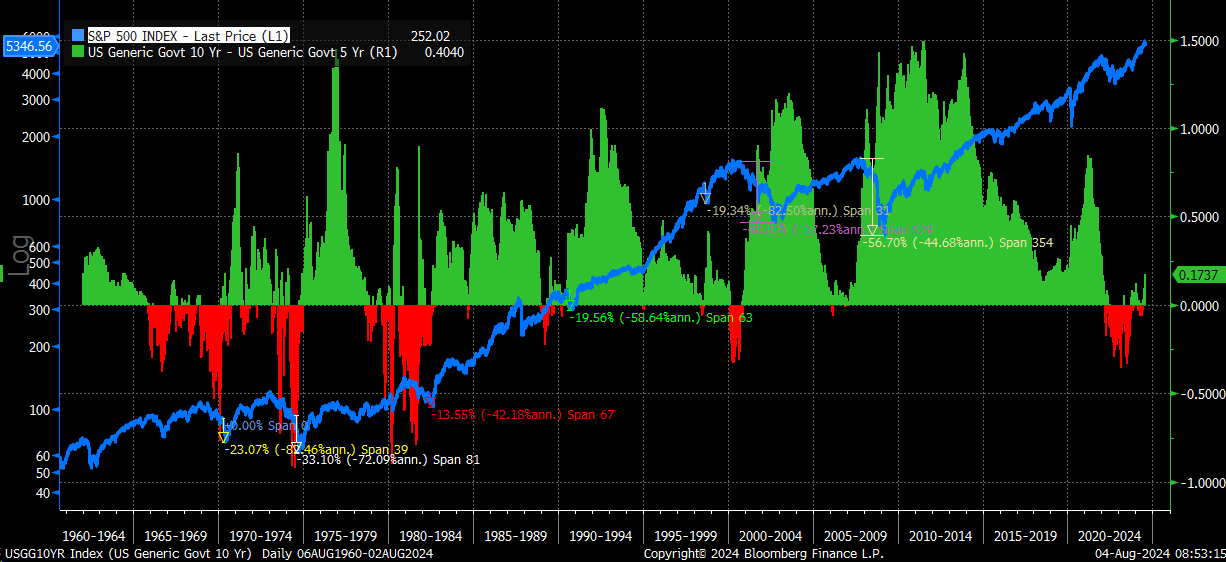

Yield Curve Spooks Bulls

Historically, when the yield curve steepens, which means it rises at a fast and constant pace, it has tended to lead to sizeable drawdowns in the US equity markets. Since I could acquire more data by using the minus the , I found that the initial thrust higher in the yield curve tended to result in nasty sell-offs in the equity market going back to around 1969.

In the following chart, I took the y/y change in the along with the change in the steepness in the 10-5 curve, and it shows fairly reasonably that when the initial thrust in the steepening of the curve pushes the index lower.

The 10-5 spread has been moving sideways from October 2023 until the end of June. The rate of acceleration has only really started since the beginning of July. If the breakout that occurred on Friday is real, the steepening process is likely to accelerate, which should continue to push equity prices lower.

Historically, the yield curve leads the , so the odds of this steepening being real seem very high.

On Friday, the S&P 500 fell out of the rising wedge pattern we have been watching for several weeks. While it hit the lower Bollinger band, the RSI is still around 38, so I wouldn’t call these conditions oversold.

Support around 5,315 was held on Friday, but a break of that level will likely start the process of filling gaps down to the 5000 level of support.

The is around 23.50, which could fuel the market’s rise if it starts dropping. However, given the volatility we have seen in recent weeks, the rule of 16 suggests an S&P 500 move of around 1.5%, which is pretty much what we have been getting the last few days. Thus, it is hard to imagine the VIX really plunging at this point.

Nvidia at Risk of More Downside

Additionally, now that we are past the Mega Cap earnings seasons implied volatility levels have reset, except for Nvidia (NASDAQ:). The surge in the VIX and the resetting of implied volatility in Mega Cap stocks will lead to further unwinding of the implied volatility dispersion trade.

The 1-month implied correlation index is still only at 21.85, proving how stupid this market was when it dropped below three on July 12. Typically, this index tops in the 40 to 50 range, so there is the potential for the index to go much higher. This tells us that the VIX probably could go higher even still.

: Gamma Squeeze Is Over Now

Now that the gamma squeeze in the is over, the rally in the IWM is over, and nearly all of the gains have vanished. There seems to be this general thought in the market that falling rates are good for small caps, but that doesn’t seem to be the case. Small caps trade with credit spreads, and rising credit spreads are bad for them. If credit spreads continue to widen, small caps will not perform well.

USD/JPY Under Pressure

The has been smashed, and it is oversold, but that may not matter because this is a trade that is unwinding, and people are just running for the exits.

In times like this, oversold may not even matter. If the USD/JPY doesn’t bounce at 146, it probably goes to 141.

But where the yen goes will likely be determined by where the goes. If the 10-year drops below 3.75%, then 3.3% is probably next. And if systematics are scrambling for exits and covering shorts, then it is possible.

So, we can see how this becomes one giant feedback loop over time: a steeper curve, lower rates, lower USD/JPY, lower equities, and higher implied volatility, further unwind of Vol dispersion. Right now, we are in the middle of a giant trade reset. The higher for longer trade is over.

#Stocks #Week #Ahead #Yield #Curve #Steepening #Puts #Global #Markets #Toes