{kind=link}

These 5 Stocks Are ‘Hiding’ Up to 6.7% in Extra Yield

Today we’ll discuss a 5.4% dividend that actually annualizes to 7%. A 5.7% payer that really dishes 12.4%. And even a headline 15% yield that is understated because the company handed out 16.1% last year.

Wait. What?

These “typos” fool the mainstream financial websites. We are discussing special dividends today. Payouts that are awarded as a bonus to regular quarterly dividends.

Only a select few firms dish specials. Sometimes, it’s thanks to a sudden influx of money. Let’s take billboard and transit display giant Outfront Media (NYSE:) which sold its Canadian business for C$410 million in cash in June.

Fast forward to November, and Outfront announced a massive 75-cent special dividend on top of its 30-cent quarterly dividend, vaulting its 12-month yield from a healthy 6.3% to a mouth-watering 10.2%. This, of course, was a one-off special—not one that we are looking to bank on annually.

We want “the other” type of special payer. The company that says it’s a one-off, but makes the payment every single year. These tend to fall into one of two camps:

- “Regular” special dividends: Some companies that produce highly variable income have adopted a “hybrid” dividend program in which they pay regular dividends at a certain baseline amount, then “top up” those distributions whenever profits or cash allow. This is becoming increasingly popular in the energy sector, where dramatic swings in energy prices sometimes force companies that solely pay regular dividends to cut their payouts, which breeds shareholder mistrust and anger.

- Sharing excess profits/cash: Some companies have less formal (but still common enough to consider) habits of sharing their wealth after bumper quarters/years.

These are the stocks that can pay us more specials in the future. Their current yields are often understated today, because specials don’t count in the annual yield calculations.

Today we’ll review five generous special payers. Mainstream financial websites list their yields between 5.4 and 15.0%. But they actually paid 7.0% to 16.1% over the past year. Let’s see if history is on pace to repeat or, at least, rhyme.

Ford (F)

Listed Dividend Yield: 5.4%

Dividend Yield With Specials: 7.0%

Ford (NYSE:) hardly needs an introduction—it’s an American automotive pioneer, and its F-Series has held the title of world’s best-selling truck for nearly a half-century.

But Ford doesn’t necessarily have the world’s happiest shareholders.

On a pure share-price basis, Ford—across a number of ups and downs—is effectively flat since 1994. That’s zero price returns—if anyone has held for two decades, their only gains as of right now have come from the dividend.

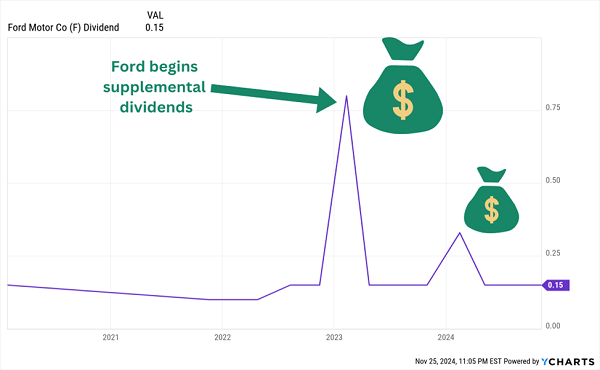

That dividend, however, is mighty interesting. Ford temporarily suspended its dividend in 2020 as COVID reared its ugly head, then brought it back at 10 cents per share for a few quarters before returning it to the pre-pandemic 15-cent level. However, instead of just raising its regular past 15 cents, Ford has spent the past two Februarys announcing special dividends—first 63 cents in 2023, then a more modest 18 cents in 2024.

That’s part of a stated plan to distribute 40%-50% of free cash flow every year—and if the regular doesn’t do the job, shareholders will get a supplemental payout. (Ford’s FCF in 2023 was $6.8 billion; it’s guiding for $7.5 billion to $8.5 billion this year, so we could assume a decently higher special in 2025 compared to 2024.)

Ford’s Payout Bounces Back with a Little Something Extra

But we need more than a nice dividend. And on that front, it’s tough to be overly positive.

Ford’s earnings are expected to decline by about 10% this year before leveling out in 2025. The company’s traditional, hybrid and fleet vehicles are generally doing well, though its electric-vehicle arm continues to struggle and deliver thick (albeit shrinking) losses. Meanwhile, while Ford should reach its expected $2 billion in cost cuts this year, warranty costs and inflation are still holding the automaker back. But F shares are cheap, at a forward price-to-earnings (P/E) of around 6.5, and a price/earnings-to-growth (PEG) of 0.65. (A stock with a PEG below 1.0 is considered undervalued.)

Equinor (EQNR)

Listed Dividend Yield: 5.7%

Dividend Yield With Specials: 12.4%

Equinor (NYSE:) is little-known to most American investors, though it will occasionally pop up on the radar of anyone seeking out great yields in the energy patch.

This Norwegian energy firm is actually two-thirds state-owned, has operations in roughly 30 countries (though most of its production comes from the Norwegian Continental Shelf), and produces roughly 2.1 million barrels of oil equivalent (boe) per day.

While it’s heavy in traditional oil and gas operations, Equinor has increasingly delved into renewables and low-carbon solutions, and has pledged to become a net-zero energy company by 2050. It owns a nearly 10% stake in Danish wind firm Orsted (CSE:), and generated 677 gigawatt hours (GWh) of renewable power in its most recent quarter.

Indeed, its focus on green energy—largely a product of Norway’s more ambitious energy targets—has hamstrung the firm compared to energy majors such as Exxon Mobil (NYSE:) and Chevron (NYSE:), which are still doggedly investing in traditional energy extraction.

Equinor also has one of the most potent special dividends. Indeed, Equinor has paid out “ordinary” and “extraordinary” dividends over the past few years. Its past three specials have been equal to the 35-cent regular distribution, with the fourth coming out to 60 cents per share. All told, those extraordinary dividends have added a whopping 6.7 points to EQNR’s yield. That’s on top of what has been an uber-generous buyback program.

EQNR Has Stepped Up Its Shareholder Reward Game for a Few Years

But this is where diving into company reports comes in handy. Seeing as how Equinor isn’t exactly a first-to-mind energy stock to most Americans, there hasn’t been much (some, but not much) reporting on that extraordinary dividend floating away. But indeed, a bullet point in the company’s 2023 full-year report noted: “Expect to conclude extraordinary cash dividend after 2024.”

The ordinary dividend will not only stay, but EQNR has pledged to grow it by 2 cents per share annually. That should result in a still-nice yield in this Norwegian energy major—but nothing approaching the wild 12.4% its most recent specials have produced.

BDCs

Business development companies (BDCs)—effectively private equity for us regular Joes—are extremely over-represented among companies offering regular-and-supplemental payouts.

Among them are:

Sixth Street Specialty Lending (TSLX)

Listed Dividend Yield: 8.9%

Dividend Yield With Specials: 10.0%

I’m on record as saying Sixth Street Specialty Lending (NYSE:) has “sterling dividend stewardship,” and that’s still the case today.

Sixth Street is a flexible provider of funding to middle-market companies, dealing in senior secured loans, mezzanine debt, non-control structured equity and common equity. A quick look at its ideal investment prospects:

- Transaction (JO:) size: $15 million-$350 million

- Company size: $50 million-$1 billion (Enterprise Value)

- EBITDA: $10 million-$250 million

Its portfolio currently sits at 115 companies spread across 15 “sector franchises,” such as sports/media/entertainment/telecom, credit market strategies, asset-based finance, and real estate. It boasts exciting names like gen-AI provider Sprinklr and parking compliance platform Passport, but also challenged retailers such as J.C. Penney and Bed Bath & Beyond.

TSLX has largely been a well-managed BDC, though last quarter, it added a non-accrual (Lithium Technologies) to bring its total to three, representing roughly 2% of investments at fair value. That’s still a low level, however—Sixth Street still has a great track record of delivering high RoE and making intelligent deals.

It also has a smart distribution system in which TSLX pays a core dividend, then distributes 50% of net investment income (NII) in excess of that core dividend as supplemental payouts, keeping the BDC from overextending itself. Over the past 12 months, specials have accounted for about 1.1 extra percentage points’ worth of yield.

TSLX Pays Out Big Regular Dividends, Small Top-Offs

But we pretty much have to overpay to buy shares. TSLX stock routinely trades at a massive premium to net asset value (NAV), and that’s still the case today—its 22% premium puts it among the five most expensive BDCs right now.

BlackRock TCP Capital Corp. (TCPC)

Listed Dividend Yield: 15.0%

Dividend Yield With Specials: 16.1%

BlackRock TCP Capital Corp (NASDAQ:) is another BDC, this one externally managed, that invests in the debt of middle-market companies with enterprise values of between $100 million and $1.5 billion.

TCPC currently has 156 companies in its portfolio, spread across a few dozen industries. But it does have a few heavier concentrations—internet software and services (~14%), software (~14%) and diversified financial services (~13%) earn double-digit weights.

Earlier this year, TCPC merged with BlackRock Capital Investment (NASDAQ:) Corp., which I previously mentioned came with a tangible benefit: a 25-basis-point reduction in base management fees, to 1.25%, bringing it a little lower than the industry midpoint. But I was also curious to see whether BlackRock TCP Capital would still keep its special dividends.

Yes, I know—what does it matter if TCPC is already doling out a massive 15%? Well, it means that TCPC isn’t necessarily overpromising on its regular dividend.

That said, the most recent dividend announcement marked a fifth consecutive regular payout of 34 cents per share, keeping it a penny shy of its pre-COVID levels and raising a little concern that TCPC’s dividend might be plateauing, at least in the short-term.

Is This as Good as It Gets?

The flip side? We can buy TCPC at a decent discount of 10% to NAV.

However, portfolio quality isn’t as ideal as it is with TSLX. Non-accruals are close to 4% at fair value, and watchlist investments increased from 2.6% to 3%. Higher debt costs are weighing on operational performance, too.

Carlyle Secured Lending (CGBD)

Listed Dividend Yield: 9.5%

Dividend Yield With Specials: 11.1%

Carlyle Secured Lending (NASDAQ:) is another externally managed BDC, and that manager is a subsidiary of multinational asset manager Carlyle Group (NASDAQ:).

CGBD invests primarily in U.S. middle market companies with between $25 million and $100 million in annual EBITDA. Its investments lean heavily toward first-lien debt (68%), though it also works through second-lien debt and equity, and it also holds investment funds. Its 128 portfolio companies cover a couple dozen industries, including healthcare/pharmaceuticals, software, aerospace/defense and leisure products/services.

CGBD came public in 2017, but it has spent its short publicly traded life putting up extremely respectable returns, including mammoth outperformance coming out of the pandemic lows.

Carlyle’s BDC Has More Than Doubled the Industry Since the Bottom

Better still? Investors have been treated to both a growing base dividend (including an 8% raise in 2024), as well as regular supplemental payouts that have boosted yield by 1.6 percentage points over the past year.

Special-Dividend Charts Are Messy, But What Matters Here Is the Trend

CGBD is building a stellar track record, but a few pockmarks are emerging. Lower short-term rates are putting downward pressure on its portfolio yield (it declined 70 bps last quarter), NAV per share and net investment income also declined in Q3, and repayments continue to run ahead of originations.

Shares are even a little overheated, at a slight premium to NAV.

Exclusive: How to Build a High-Yield Monthly Income Stream WITHOUT Overpaying

You wouldn’t buy a car for 24% above MSRP, and COVID-era homebuyers can tell you how painful it is to pay 24% above the asking price. So why would you kneecap yourself by purchasing a fund for 24% above NAV—especially when there are still plenty of reasonably priced monthly payers ripe for the picking?

Case in point? My “8%+ Monthly Payer Portfolio” is chock full of reasonably priced “steady Eddie” stocks that deliver sky-high yields and beautifully boring businesses that won’t give you nausea over the years … and meaningful price upside, which means we can keep growing our nest eggs well after we’ve hit the retirement button.

This is how we win in retirement.

Many retirement plans build your nest egg, only to turn around and ask you to bleed that same nest egg dry as you age. But the income this portfolio can generate is so rich, it can sustain a retirement on dividends alone.

Here’s the math: If you have a million dollars to work with, an 8% baseline will net you $80,000 a year.

But even if you’re well behind on your retirement savings—let’s say you only have $500,000 to work with—you’ll still generate a roughly $40,000 annual income stream.

That’s $4,000 every month in regular income checks!

Can your current portfolio deliver that level of income? If not, it’s time to make a change.

Disclosure: Brett Owens and Michael Foster are contrarian income investors who look for undervalued stocks/funds across the U.S. markets. Click here to learn how to profit from their strategies in the latest report, “7 Great Dividend Growth Stocks for a Secure Retirement.”

#Stocks #Hiding #Extra #Yield