{kind=link}

Who’s better off and who’s worse off four years on from the outbreak of COVID? The financial picture might surprise you

A lot has happened to the economy since COVID struck, and reading the economic tea leaves has become more difficult.

Many of the gains for many Australians in 2020 and 2021 were artificial and didn’t last. The COVID Supplement temporarily doubled JobSeeker, for example. JobKeeper paid workers what their employers could not.

As these measures have been unwound, the gains have been unwound, making it more difficult than usual to separate the economic signal from the noise.

But in a study just published in the the ANU Centre for Social Policy Research journal POLIS@ANU we have made an attempt.

We wanted to find out which kinds of households are expected to be financially better off and which worse off five years on from the outbreak of COVID, comparing 2024 with 2019.

We’ve adjusted incomes for living costs

We have examined incomes after adjusting for changes in living costs. This means that if a household’s after-tax income increased by 20% but its cost of living also increased by 20%, we have regarded its financial living standard as unchanged.

The tool we used was the ANU PolicyMod model of the Australian tax and transfer system, Australian Bureau of Statistics data on employment, demographics and prices and wages, and government data on tax and payments.

We have also taken account of the income tax cuts and changes to payments that begin next month. Our estimates for December 2024 are projections based on the assumptions in the budget about incomes and prices.

We find overall living standards increased from 2019 to 2021 but then fell sharply in 2022 with a further small fall in 2023. Overall living standards were 0.6% lower in December 2023 than in December 2019.

This year they are expected to climb to be 1.3% higher than December 2019.

But it’s an overall picture that glosses over the full story.

Gains for high earners, low earners

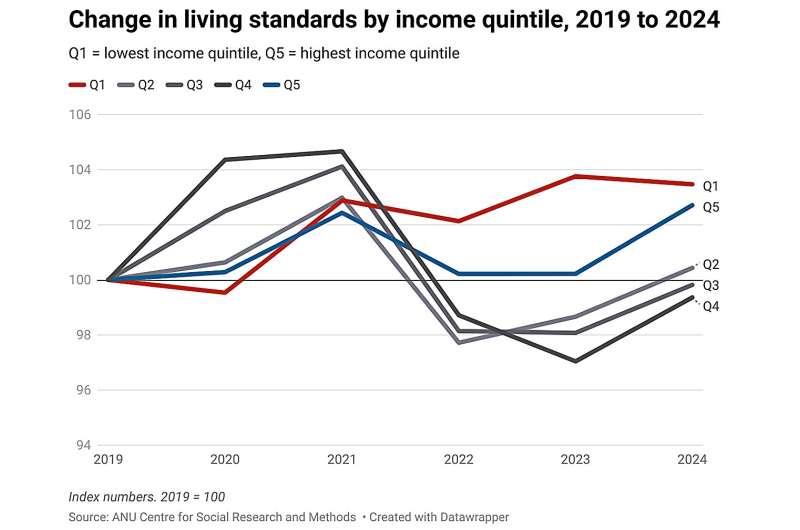

The only groups whose living standards grew significantly over the period were households on the very lowest and the very highest incomes.

We divided households into five “quintiles”. The lowest-income fifth we called Quintile 1. The highest-income fifth we called Quintile 5.

The Quintile 1 living standard grew 3.5%. The Quintile 5 living standard grew 2.7%.

In contrast, the living standard of the second-lowest quintile barely grew, and the living standards of the middle and upper-middle quintiles actually fell.

The living standards of middle and upper-middle-income Australians were lower in early 2024 than they had been in 2019.

Low-income households did relatively well partly because their payments were indexed to inflation. High-income households did well partly because they had investments that did well.

Where middle earners did badly, it was in large measure because they had mortgages. Where they did well, it seems to have been because they were outright homeowners and had other sources of investment income.

Losses for the mortgaged middle

The living standards of mortgaged households fell 5.6% between 2019 and December 2024.

In contrast, the living standards of renters climbed 2.9%, while the living standards of outright owners climbed 8.5%

On sources of income, the living standards of households whose main source of income was “other” (including investments) grew an astounding 15.8%.

In contrast, the living standards of households that relied on wages and the standards of those that relied on government benefits changed little.

The living standards of households headed by employers fell almost 10%.

Possibly for related reasons, older Australians have done much better than working-aged Australians, and the youngest did better than the middle-aged.

We also tried dividing households by “financial well-being”, a measure made up of income, wealth, housing tenure, age, disability and family type based on their statistical associations with the Bureau of Statistics measure of “financial stress”.

The bureau’s measure includes inability to raise emergency funds within a week and to pay bills on time.

Again, we divided households into quintiles. We called the fifth with the least well-being Quintile 1; the fifth with the highest well-being Quintile 5.

The most well-off are better off

The households with the highest well-being did the best, finding themselves 6.2% better off by 2024.

Those who did the worst were those with the second-highest and middle wellbeings, who found themselves about 3% worse off.

Those with the least well-being were 2.8% better off.

Overall, we did not find that household living standards have dropped remarkably since the onset of COVID.

But we can understand why some Australians, particularly middle-income Australians with mortgages and middle-aged Australians, feel they have.

They did badly in 2022 and 2023 as mortgages rose. Less advantaged and more advantaged Australians did better.

This article is republished from The Conversation under a Creative Commons license. Read the original article.![]()

Citation:

Who’s better off and who’s worse off four years on from the outbreak of COVID? The financial picture might surprise you (2024, June 9)

retrieved 9 June 2024

from

This document is subject to copyright. Apart from any fair dealing for the purpose of private study or research, no

part may be reproduced without the written permission. The content is provided for information purposes only.

Science, Physics News, Science news, Technology News, Physics, Materials, Nanotech, Technology, Science

#Whos #whos #worse #years #outbreak #COVID #financial #picture #surprise